Over the last six months, Apogee’s shares have sunk to $34.59, producing a disappointing 18.4% loss - a stark contrast to the S&P 500’s 17.2% gain. This might have investors contemplating their next move.

Is there a buying opportunity in Apogee, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Do We Think Apogee Will Underperform?

Even though the stock has become cheaper, we're swiping left on Apogee for now. Here are three reasons why APOG doesn't excite us and a stock we'd rather own.

1. Long-Term Revenue Growth Disappoints

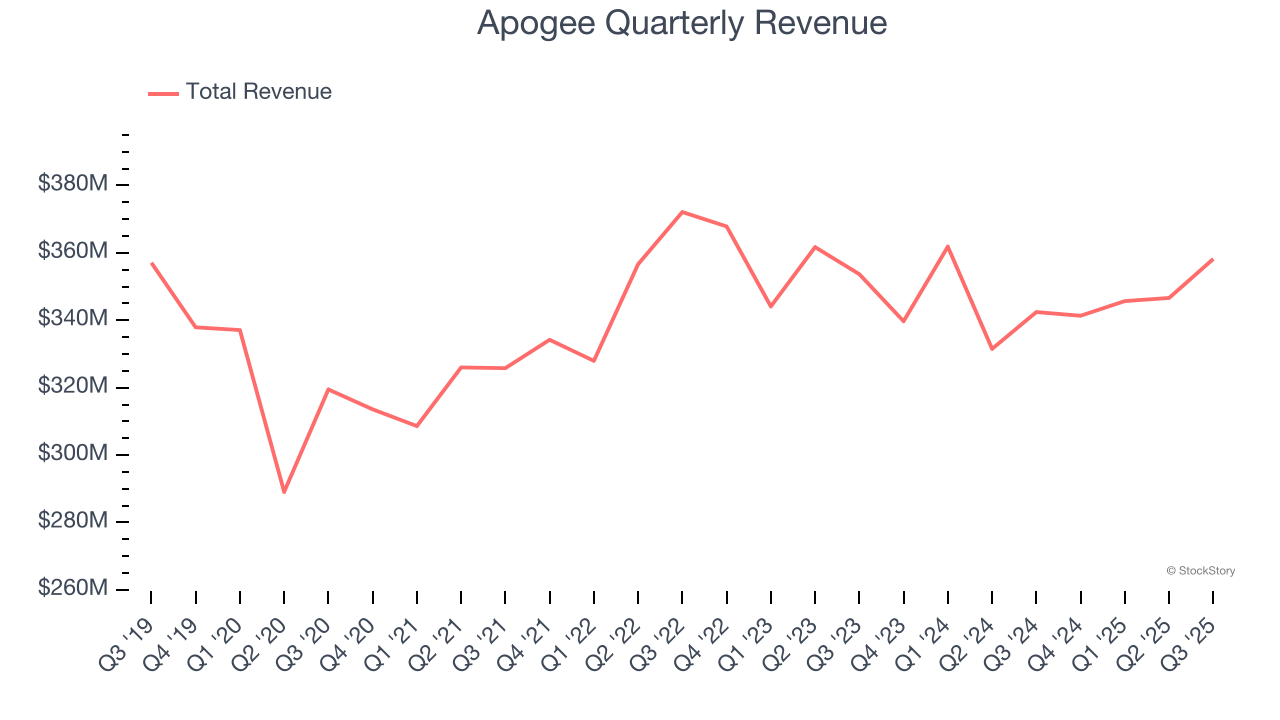

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Apogee grew its sales at a sluggish 1.6% compounded annual growth rate. This fell short of our benchmarks.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Apogee’s revenue to rise by 1%. While this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

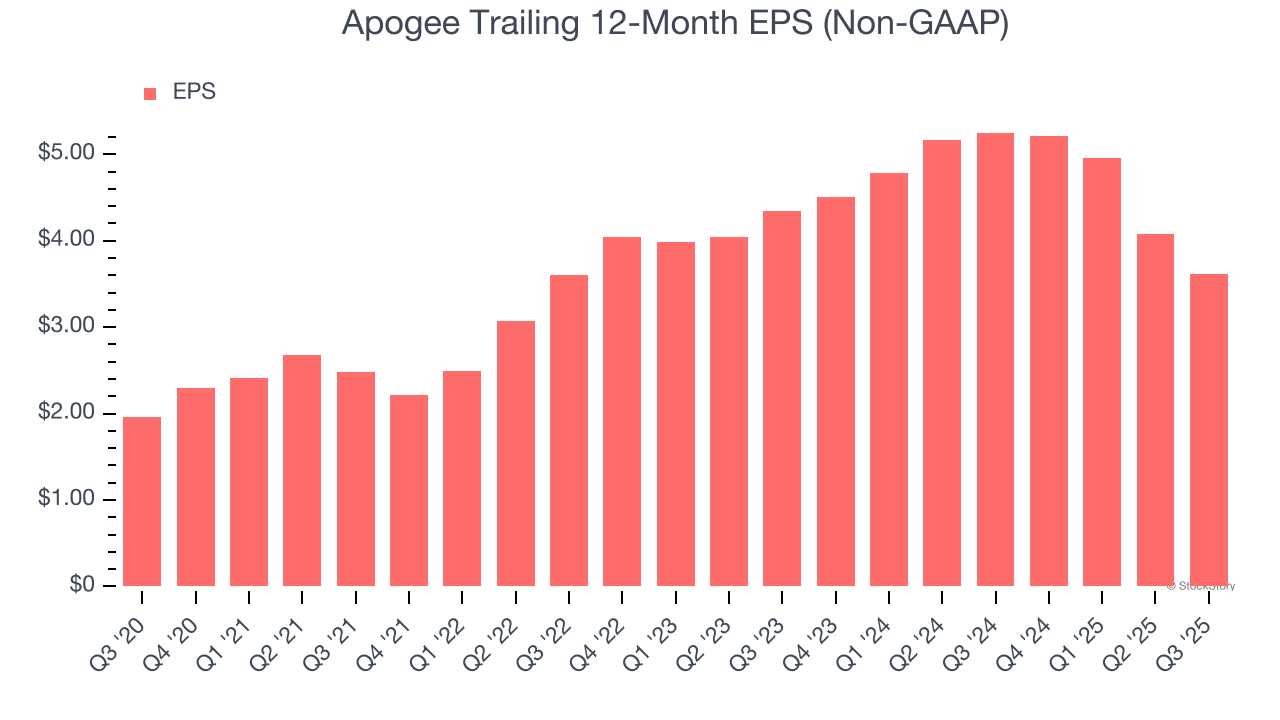

3. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Apogee, its EPS declined by more than its revenue over the last two years, dropping 8.7%. This tells us the company struggled to adjust to shrinking demand.

Final Judgment

We see the value of companies helping their customers, but in the case of Apogee, we’re out. After the recent drawdown, the stock trades at 8.5× forward P/E (or $34.59 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. Let us point you toward one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

Fresh US-China trade tensions just tanked stocks—but strong bank earnings are fueling a sharp rebound. Don’t miss the bounce.

Don’t let fear keep you from great opportunities and take a look at Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.