Everest Group has been treading water for the past six months, holding steady at $343.50. The stock also fell short of the S&P 500’s 8.6% gain during that period.

Is now the time to buy EG? Find out in our full research report, it’s free.

Why Does EG Stock Spark Debate?

Rebranded from Everest Re in 2023 to reflect its evolution beyond just reinsurance, Everest Group (NYSE: EG) underwrites property and casualty reinsurance and insurance worldwide, serving insurance companies, corporations, and other clients across six continents.

Two Positive Attributes:

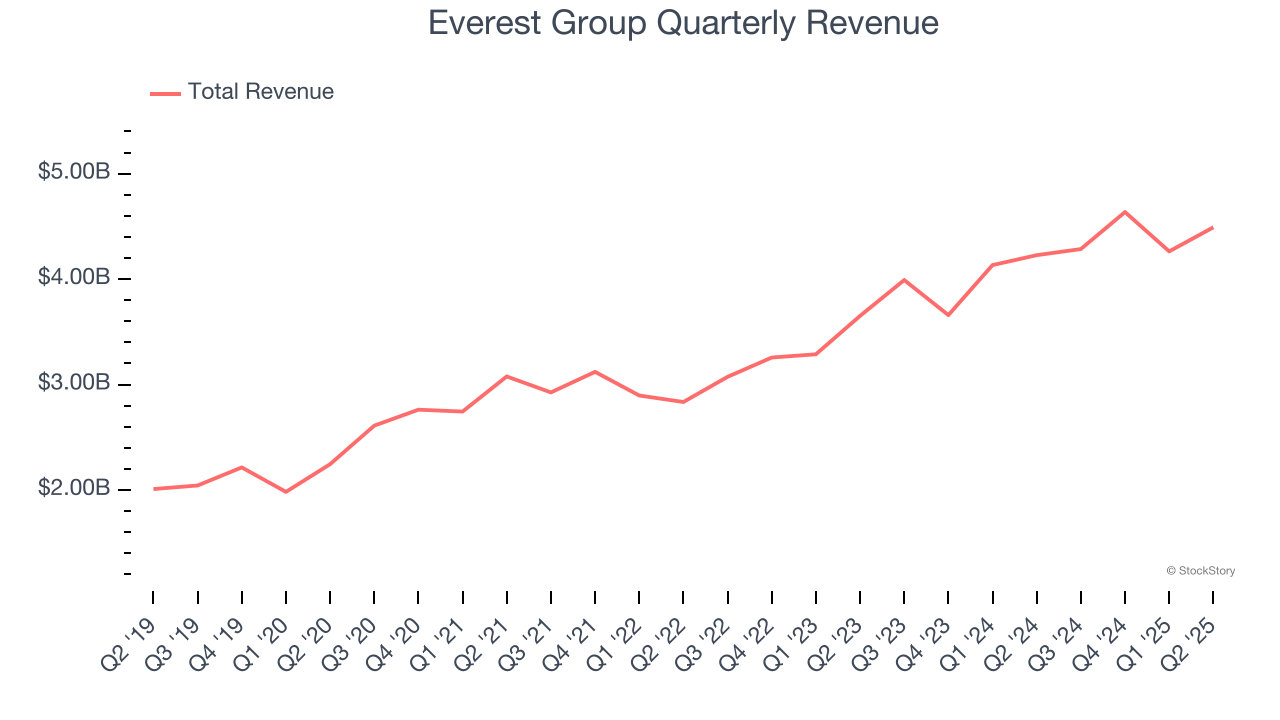

1. Skyrocketing Revenue Shows Strong Momentum

In general, insurance companies earn revenue from three primary sources. The first is the core insurance business itself, often called underwriting and represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services.

Thankfully, Everest Group’s 15.8% annualized revenue growth over the last five years was incredible. Its growth beat the average insurance company and shows its offerings resonate with customers.

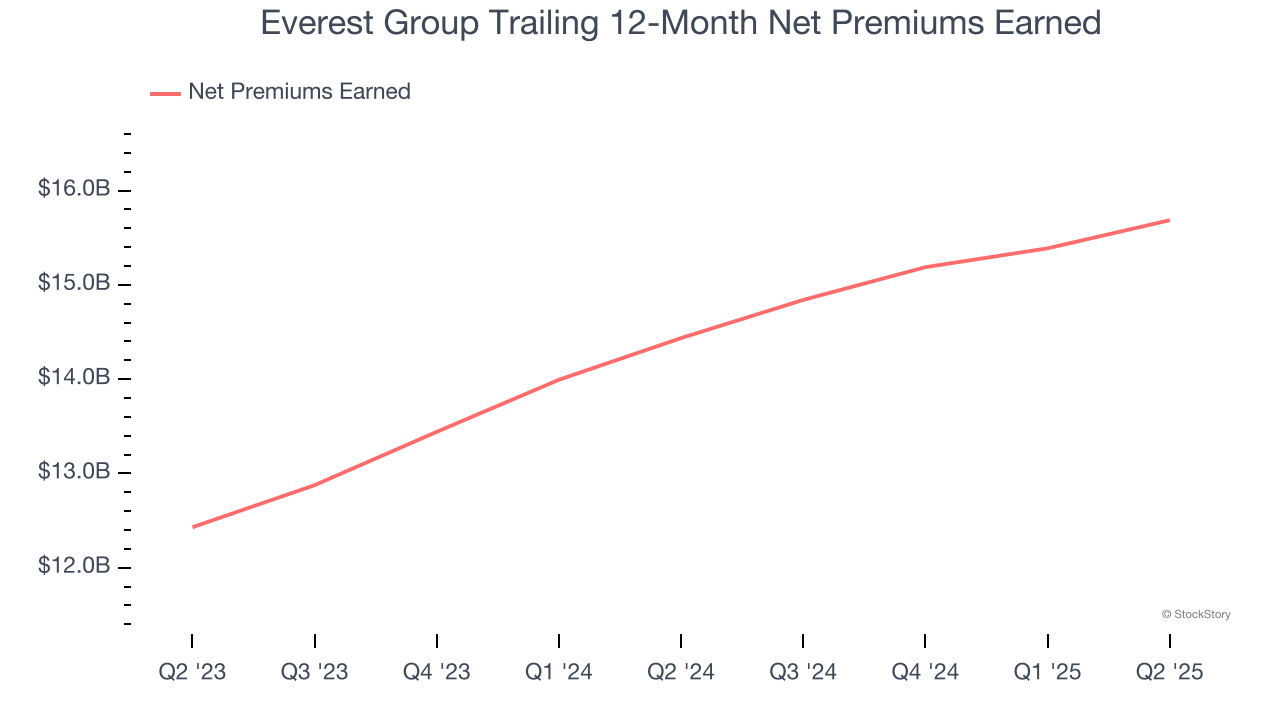

2. Net Premiums Earned Skyrocket, Fueling Growth Opportunities

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore net of what’s ceded to reinsurers as a risk mitigation and transfer strategy.

Everest Group’s net premiums earned has grown at a 14% annualized rate over the last five years, better than the broader insurance industry.

One Reason to be Careful:

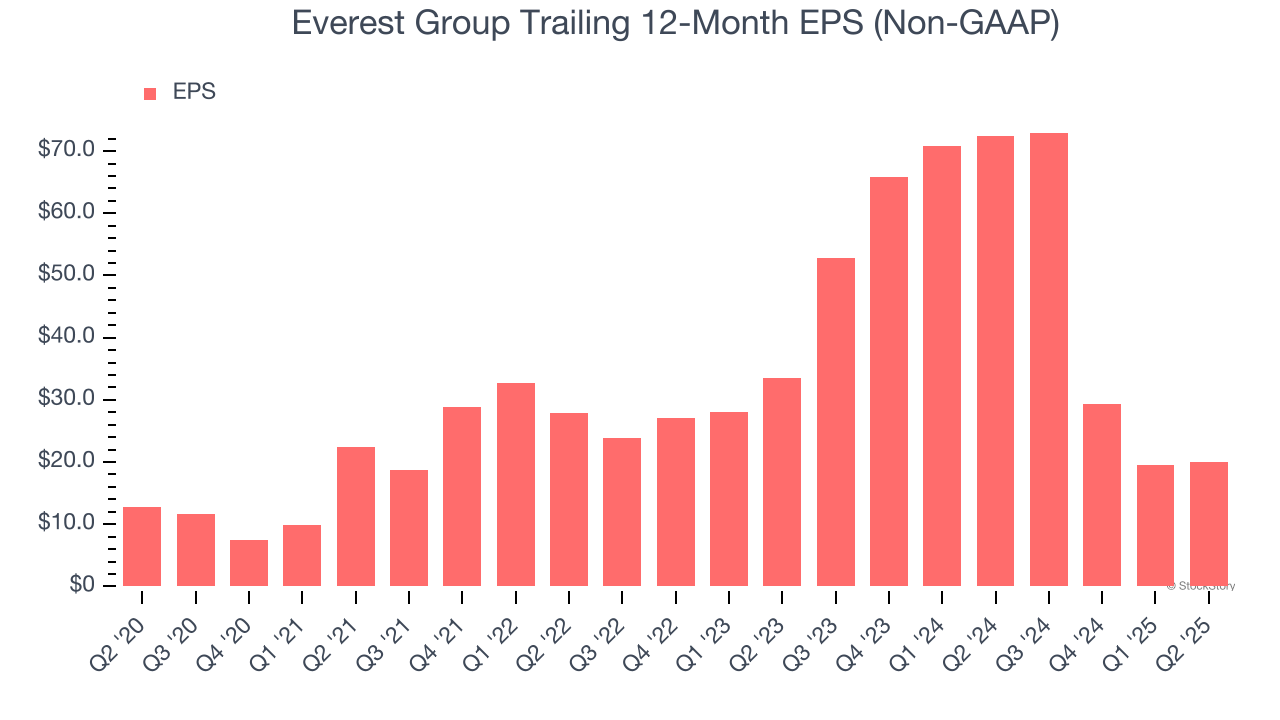

EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Everest Group’s EPS grew at an unimpressive 9.6% compounded annual growth rate over the last five years, lower than its 15.8% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Everest Group’s merits more than compensate for its flaws. With its shares underperforming the market lately, the stock trades at 0.9× forward P/B (or $343.50 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.