Visual content marketplace Getty Images (NYSE: GETY) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 14.1% year on year to $282.3 million. On the other hand, the company’s full-year revenue guidance of $968 million at the midpoint came in 0.5% below analysts’ estimates. Its non-GAAP loss of $0.01 per share was $0.03 below analysts’ consensus estimates.

Is now the time to buy Getty Images? Find out by accessing our full research report, it’s free.

Getty Images (GETY) Q4 CY2025 Highlights:

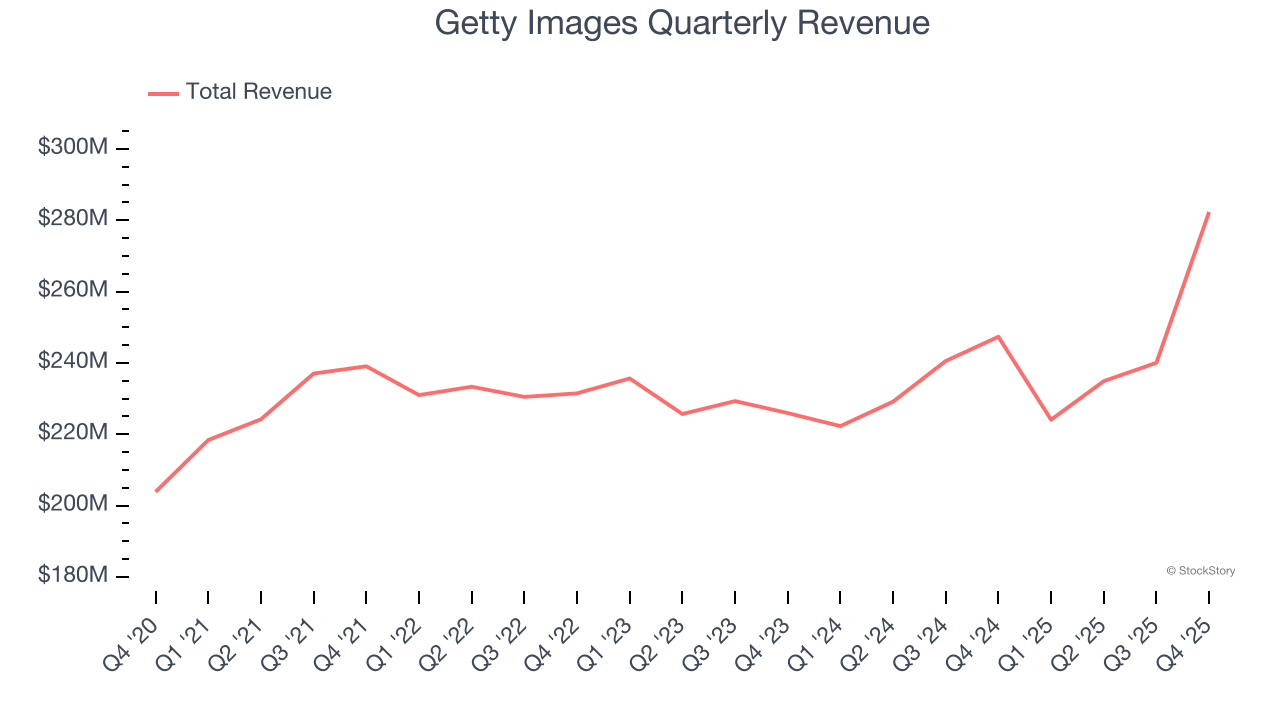

- Revenue: $282.3 million vs analyst estimates of $245.6 million (14.1% year-on-year growth, 15% beat)

- Adjusted EPS: -$0.01 vs analyst estimates of $0.02 ($0.03 miss)

- Adjusted EBITDA: $104.1 million vs analyst estimates of $74.7 million (36.9% margin, 39.3% beat)

- EBITDA guidance for the upcoming financial year 2026 is $287 million at the midpoint, below analyst estimates of $304.5 million

- Operating Margin: -8.5%, down from 14.5% in the same quarter last year

- Free Cash Flow Margin: 2.7%, down from 9.9% in the same quarter last year

- Market Capitalization: $303.2 million

“In our 30th anniversary year we delivered record revenue, with growth across both Creative and Editorial,” said Craig Peters, Chief Executive Officer at Getty Images.

Company Overview

With a vast library of over 562 million visual assets documenting everything from breaking news to iconic historical moments, Getty Images (NYSE: GETY) is a global visual content marketplace that licenses photos, videos, illustrations, and music to businesses, media outlets, and creative professionals.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $981.3 million in revenue over the past 12 months, Getty Images is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels.

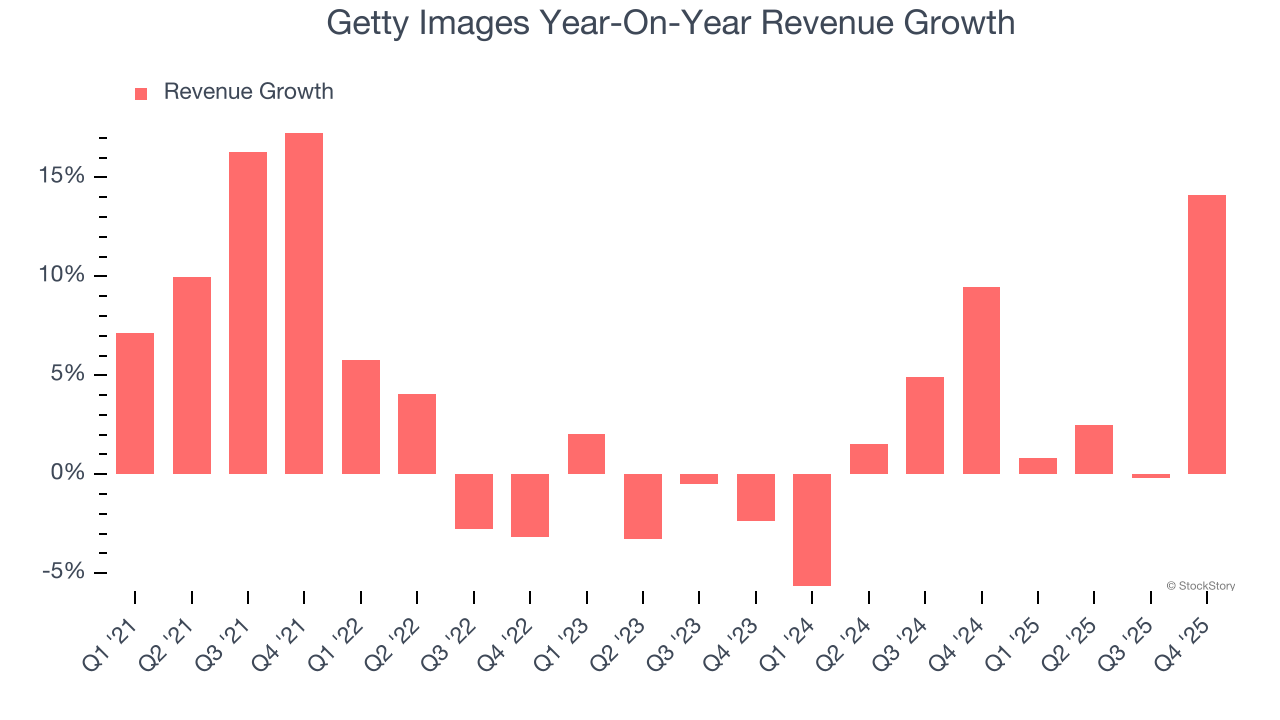

As you can see below, Getty Images’s sales grew at a tepid 3.8% compounded annual growth rate over the last five years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Getty Images’s annualized revenue growth of 3.5% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Getty Images reported year-on-year revenue growth of 14.1%, and its $282.3 million of revenue exceeded Wall Street’s estimates by 15%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

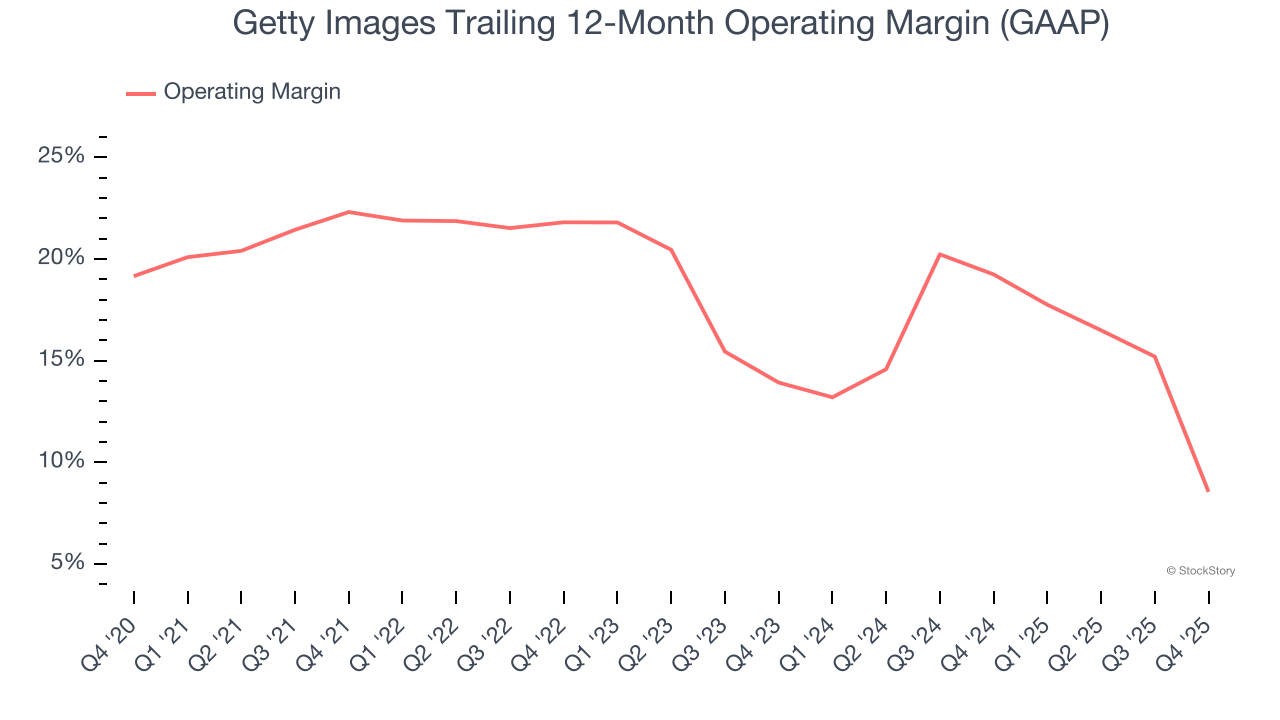

Getty Images has been an efficient company over the last five years. It was one of the more profitable businesses in the business services sector, boasting an average operating margin of 17.1%.

Analyzing the trend in its profitability, Getty Images’s operating margin decreased by 13.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Getty Images generated an operating margin profit margin of negative 8.5%, down 23 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

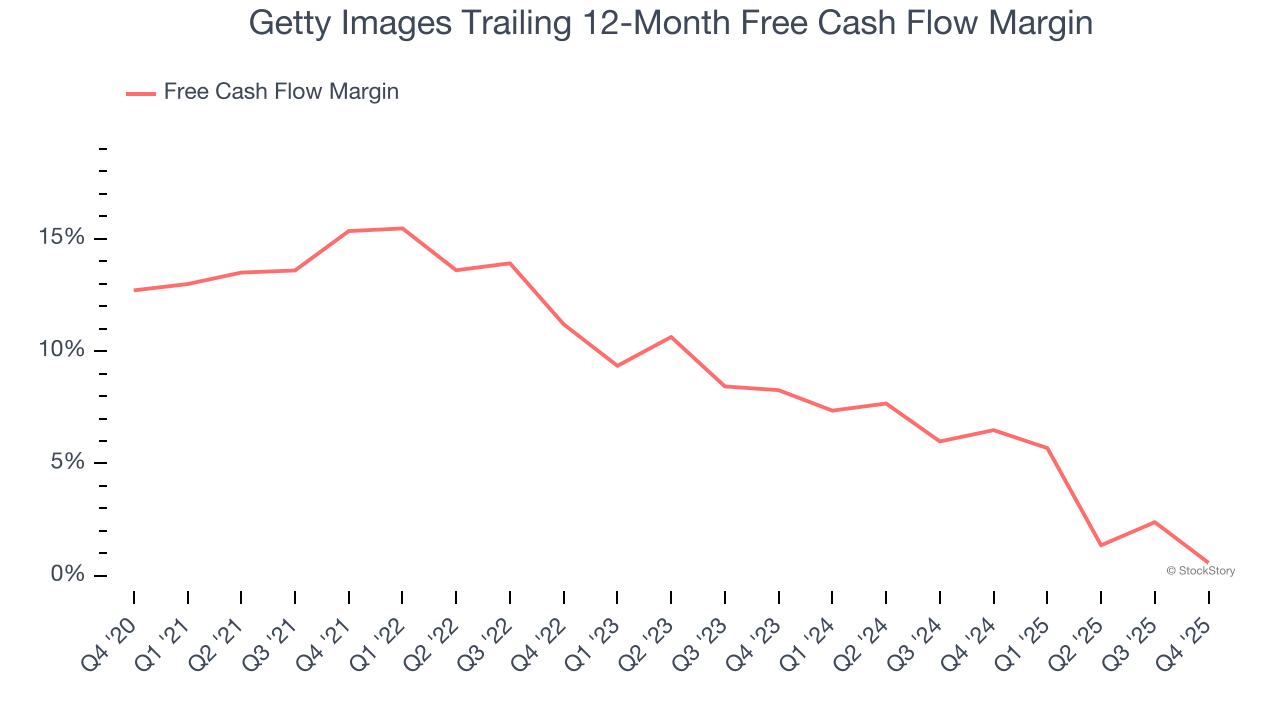

Getty Images has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.3% over the last five years, better than the broader business services sector.

Taking a step back, we can see that Getty Images’s margin dropped by 14.8 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Getty Images’s free cash flow clocked in at $7.67 million in Q4, equivalent to a 2.7% margin. The company’s cash profitability regressed as it was 7.2 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

Key Takeaways from Getty Images’s Q4 Results

We were impressed by how significantly Getty Images blew past analysts’ revenue expectations this quarter. On the other hand, its EPS was in line and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $0.77 immediately after reporting.

Is Getty Images an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).