agilon health trades at $26.45 per share and has stayed right on track with the overall market, gaining 9.6% over the last six months. At the same time, the S&P 500 has returned 5.1%.

Is there a buying opportunity in agilon health, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is agilon health Not Exciting?

We don't have much confidence in agilon health. Here are three reasons there are better opportunities than AGL and a stock we'd rather own.

1. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect agilon health’s revenue to drop by 8%, a decrease from its 37.2% annualized growth for the past five years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

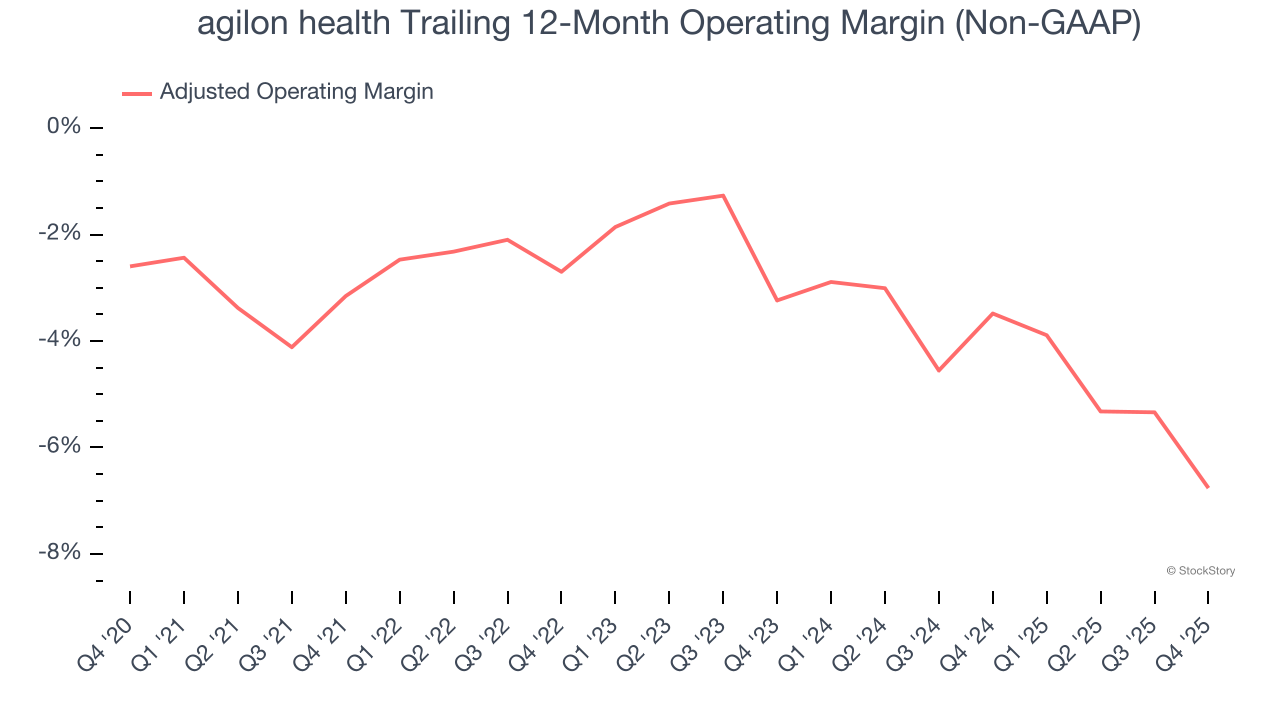

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Analyzing the trend in its profitability, agilon health’s adjusted operating margin decreased by 3.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. agilon health’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its adjusted operating margin for the trailing 12 months was negative 6.8%.

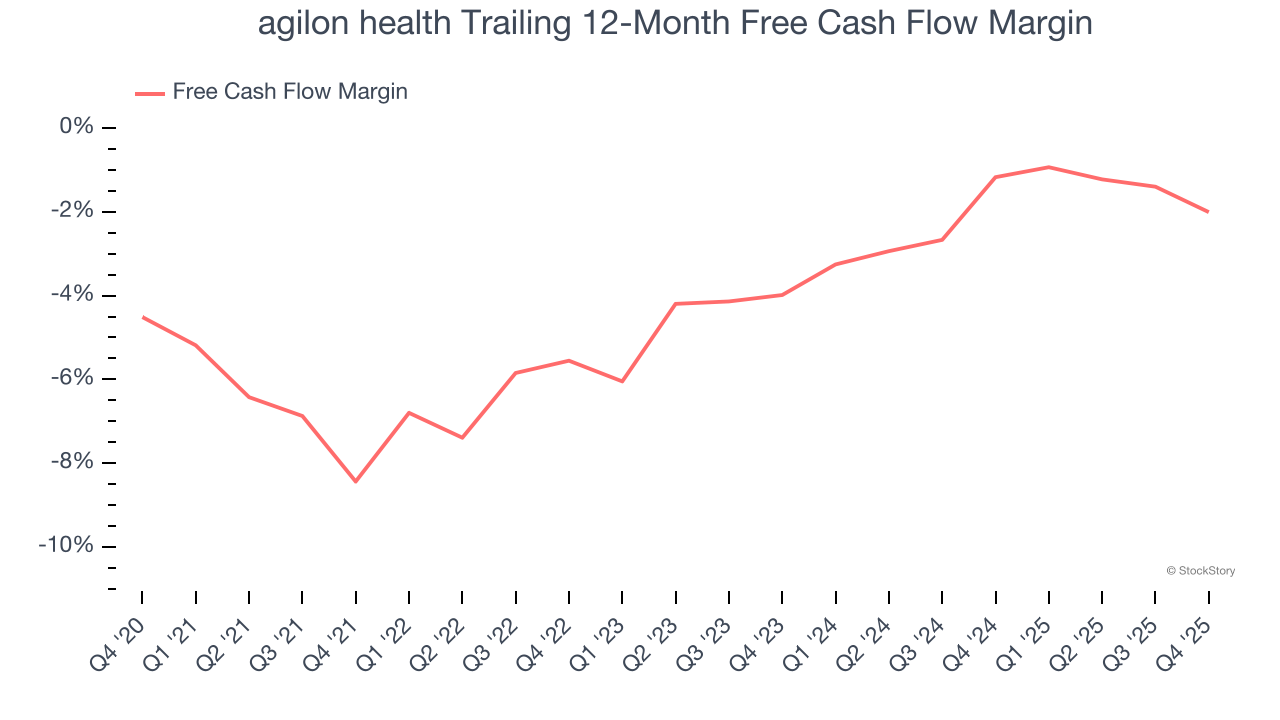

3. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

agilon health’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 3.2%. This means it lit $3.19 of cash on fire for every $100 in revenue.

Final Judgment

agilon health isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at $26.45 per share (or a forward price-to-sales ratio of 0.1×). The market typically values companies like agilon health based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. We’d suggest looking at one of our all-time favorite software stocks.

Stocks We Like More Than agilon health

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.