Diversified solutions provider Matthews International (NASDAQ: MATW) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, but sales fell by 39.5% year on year to $258.6 million. Its non-GAAP profit of $0.37 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Matthews? Find out by accessing our full research report, it’s free.

Matthews (MATW) Q1 CY2026 Highlights:

- Revenue: $258.6 million vs analyst estimates of $253.7 million (39.5% year-on-year decline, 2% beat)

- Adjusted EPS: $0.37 vs analyst estimates of $0.15 (significant beat)

- Adjusted EBITDA: $44.74 million vs analyst estimates of $40.36 million (17.3% margin, 10.9% beat)

- EBITDA guidance for the full year is $180 million at the midpoint, in line with analyst expectations

- Operating Margin: -1.2%, down from 0.8% in the same quarter last year

- Free Cash Flow was -$19.48 million compared to -$2.41 million in the same quarter last year

- Market Capitalization: $864.7 million

Company Overview

Originally a death care company, Matthews International (NASDAQ: MATW) is a diversified company offering ceremonial services, brand solutions and industrial technologies.

Revenue Growth

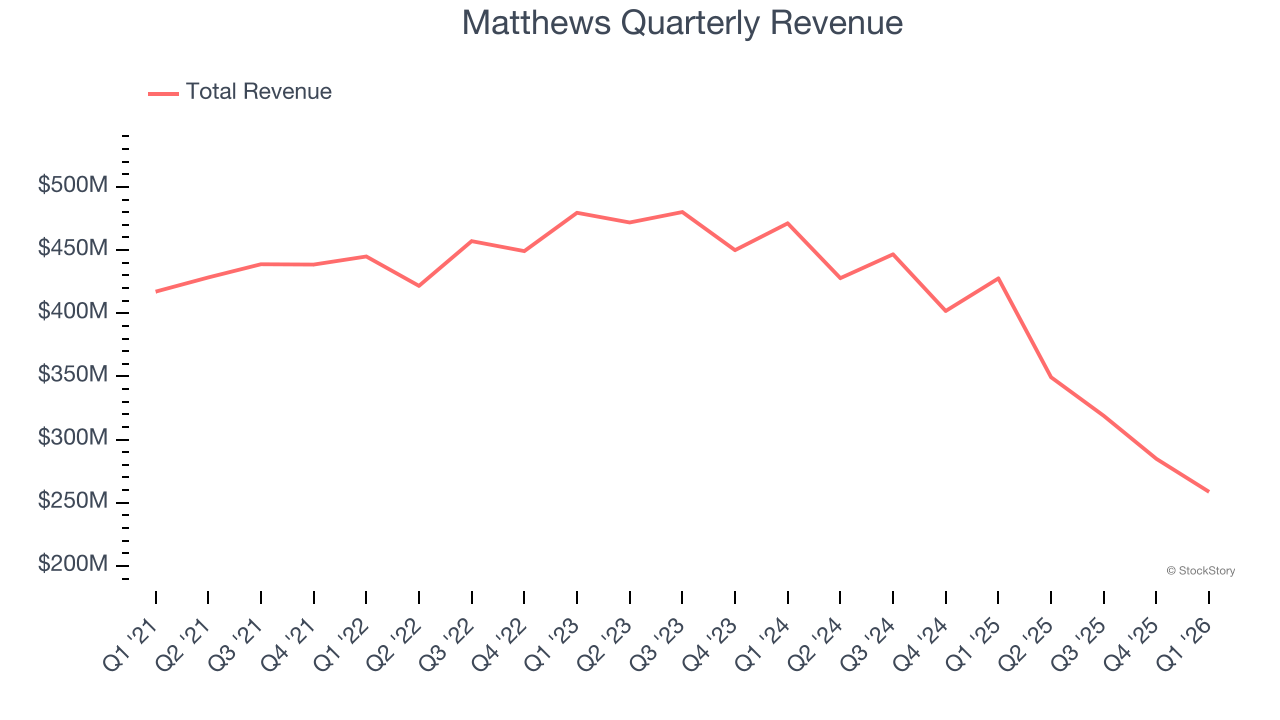

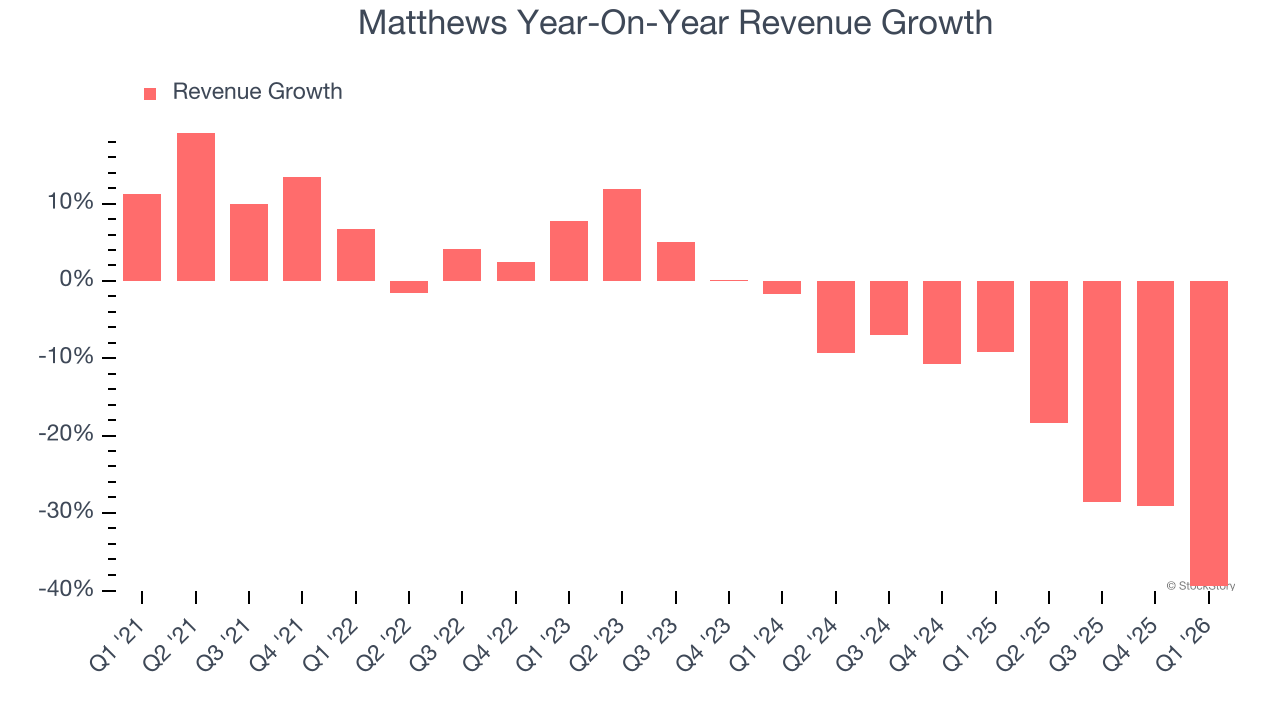

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Matthews’s demand was weak and its revenue declined by 5% per year. This wasn’t a great result and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Matthews’s recent performance shows its demand remained suppressed as its revenue has declined by 19.6% annually over the last two years.

This quarter, Matthews’s revenue fell by 39.5% year on year to $258.6 million but beat Wall Street’s estimates by 2%.

Looking ahead, sell-side analysts expect revenue to decline by 17.3% over the next 12 months. While this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

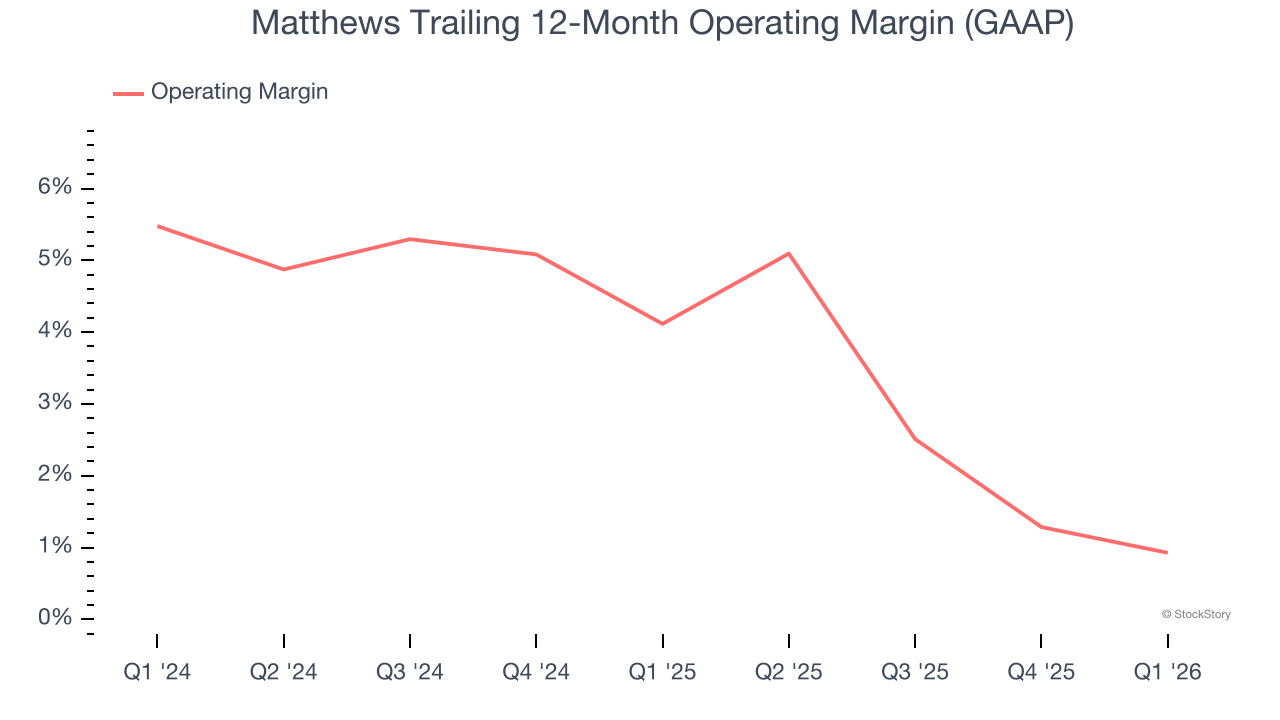

Operating Margin

Matthews’s operating margin has been trending down over the last 12 months and averaged 2.8% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Matthews generated an operating margin profit margin of negative 1.2%, down 2 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

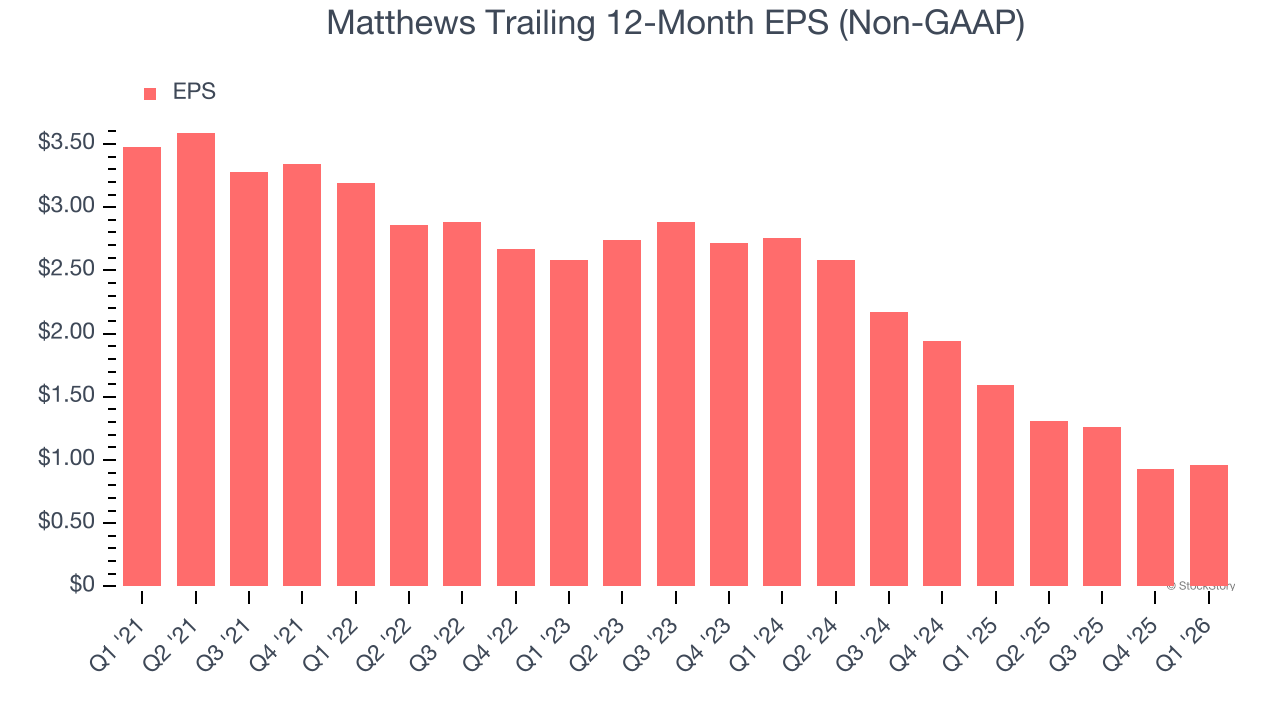

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Matthews, its EPS declined by 22.7% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q1, Matthews reported adjusted EPS of $0.37, up from $0.34 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Matthews’s Q1 Results

It was good to see Matthews beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its adjusted operating income missed. Overall, this print had some key positives. The stock traded up 4.8% to $29.91 immediately following the results.

So do we think Matthews is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).