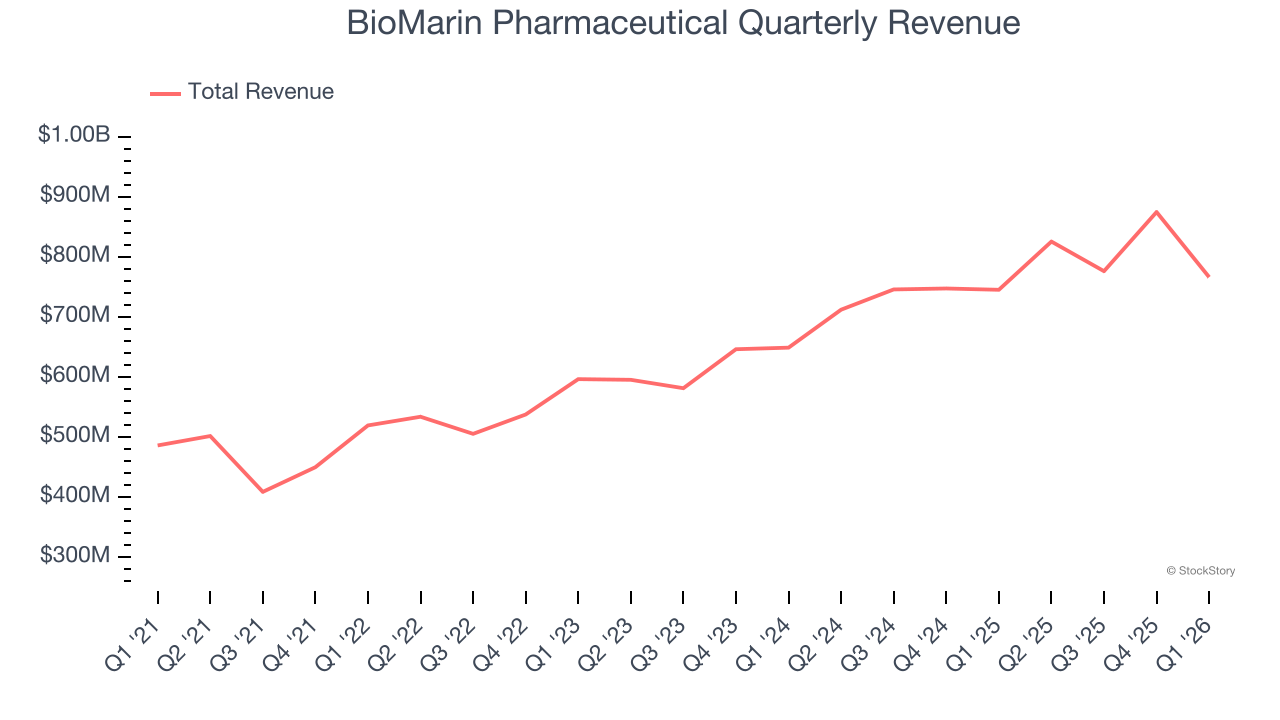

Biotech company BioMarin Pharmaceutical (NASDAQ: BMRN) missed Wall Street’s revenue expectations in Q1 CY2026 as sales rose 2.8% year on year to $766.2 million. On the other hand, the company’s full-year revenue guidance of $3.88 billion at the midpoint came in 1.2% above analysts’ estimates. Its non-GAAP profit of $0.76 per share was 16.9% below analysts’ consensus estimates.

Is now the time to buy BioMarin Pharmaceutical? Find out by accessing our full research report, it’s free.

BioMarin Pharmaceutical (BMRN) Q1 CY2026 Highlights:

- Revenue: $766.2 million vs analyst estimates of $776 million (2.8% year-on-year growth, 1.3% miss)

- Adjusted EPS: $0.76 vs analyst expectations of $0.91 (16.9% miss)

- Adjusted EBITDA: $189.5 million vs analyst estimates of $150.8 million (24.7% margin, 25.6% beat)

- The company lifted its revenue guidance for the full year to $3.88 billion at the midpoint from $3.38 billion, a 14.8% increase

- Management lowered its full-year Adjusted EPS guidance to $4.95 at the midpoint, a 2% decrease

- Operating Margin: 16.9%, down from 30% in the same quarter last year

- Free Cash Flow Margin: 26.1%, up from 21.2% in the same quarter last year

- Market Capitalization: $10.45 billion

"With the acquisition of Amicus Therapeutics complete, the addition of GALAFOLD and POMBILITI + OPFOLDA to our commercial portfolio allows us to reach patients with Fabry and Pompe diseases and meaningfully strengthens and accelerates our near-to-mid-term growth rates," said Alexander Hardy, President and Chief Executive Officer of BioMarin.

Company Overview

Pioneering treatments for conditions that often had no previous therapeutic options, BioMarin Pharmaceutical (NASDAQ: BMRN) develops and commercializes therapies that address the root causes of rare genetic disorders, particularly those affecting children.

Revenue Growth

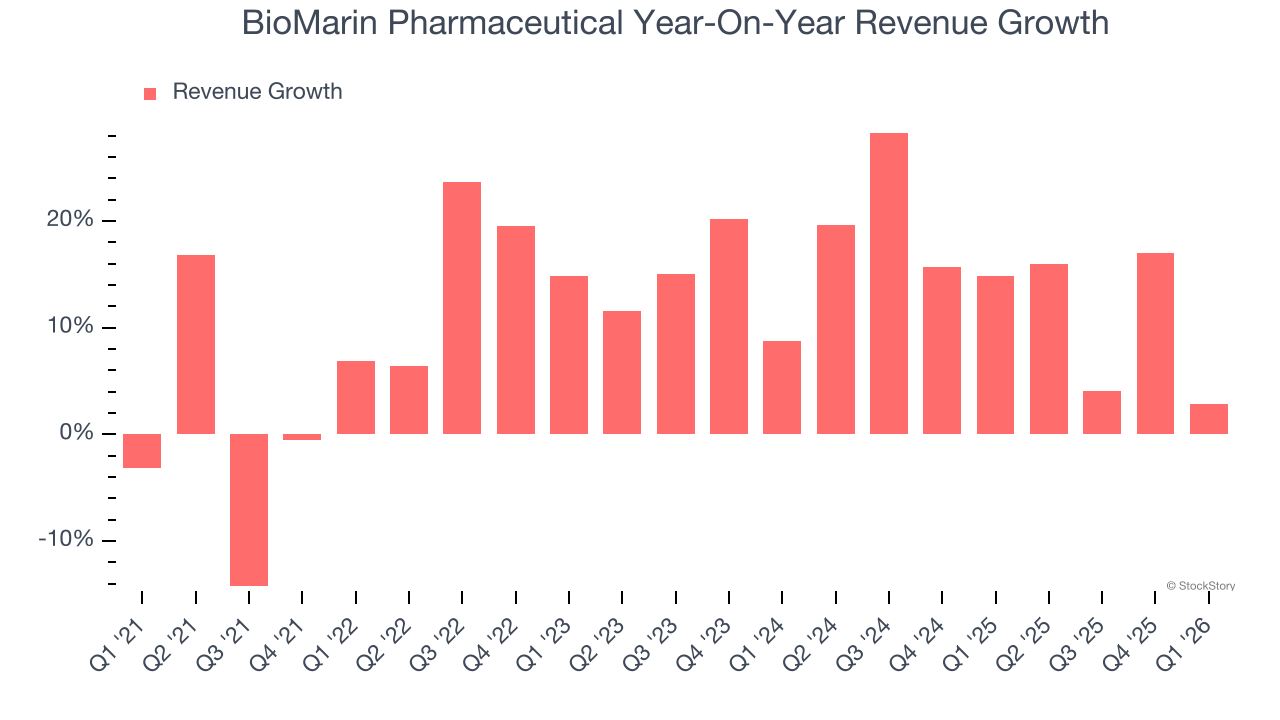

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, BioMarin Pharmaceutical’s sales grew at a decent 11.9% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. BioMarin Pharmaceutical’s annualized revenue growth of 14.5% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, BioMarin Pharmaceutical’s revenue grew by 2.8% year on year to $766.2 million, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 19.5% over the next 12 months, an improvement versus the last two years. This projection is healthy and suggests its newer products and services will spur better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

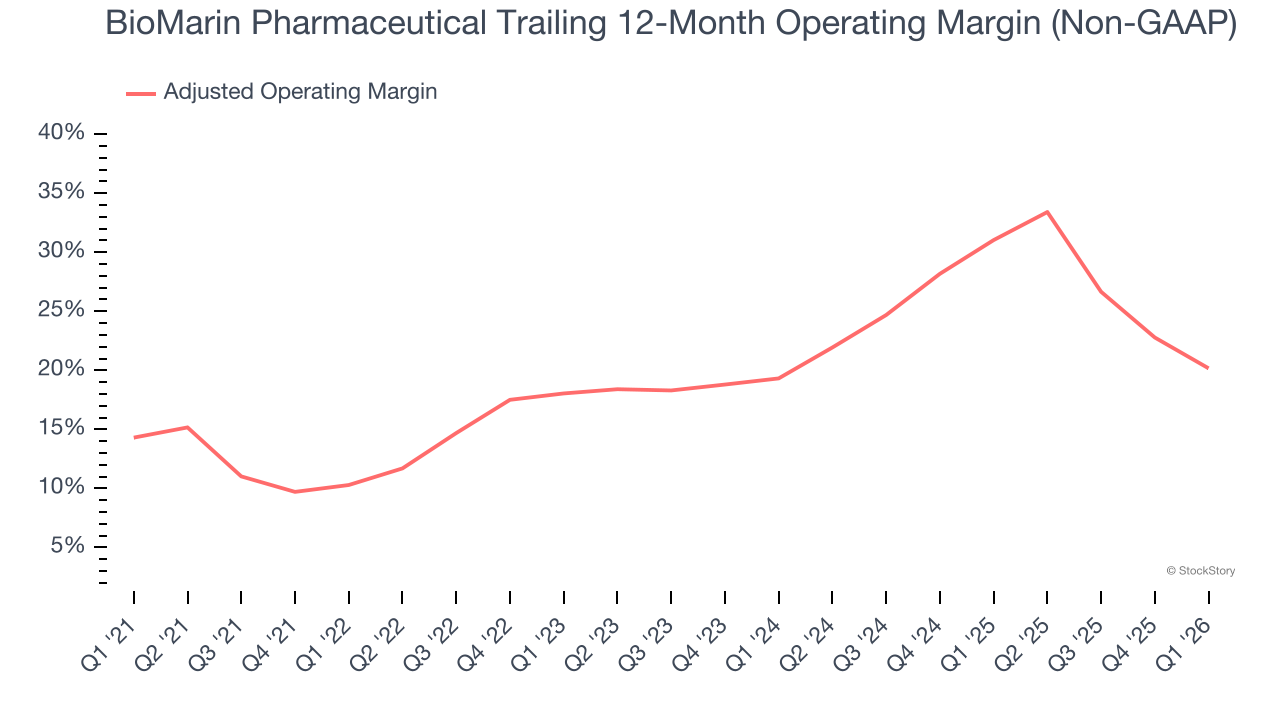

BioMarin Pharmaceutical has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 20.7%.

Analyzing the trend in its profitability, BioMarin Pharmaceutical’s adjusted operating margin rose by 9.9 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, BioMarin Pharmaceutical generated an adjusted operating margin profit margin of 24.3%, down 11.4 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

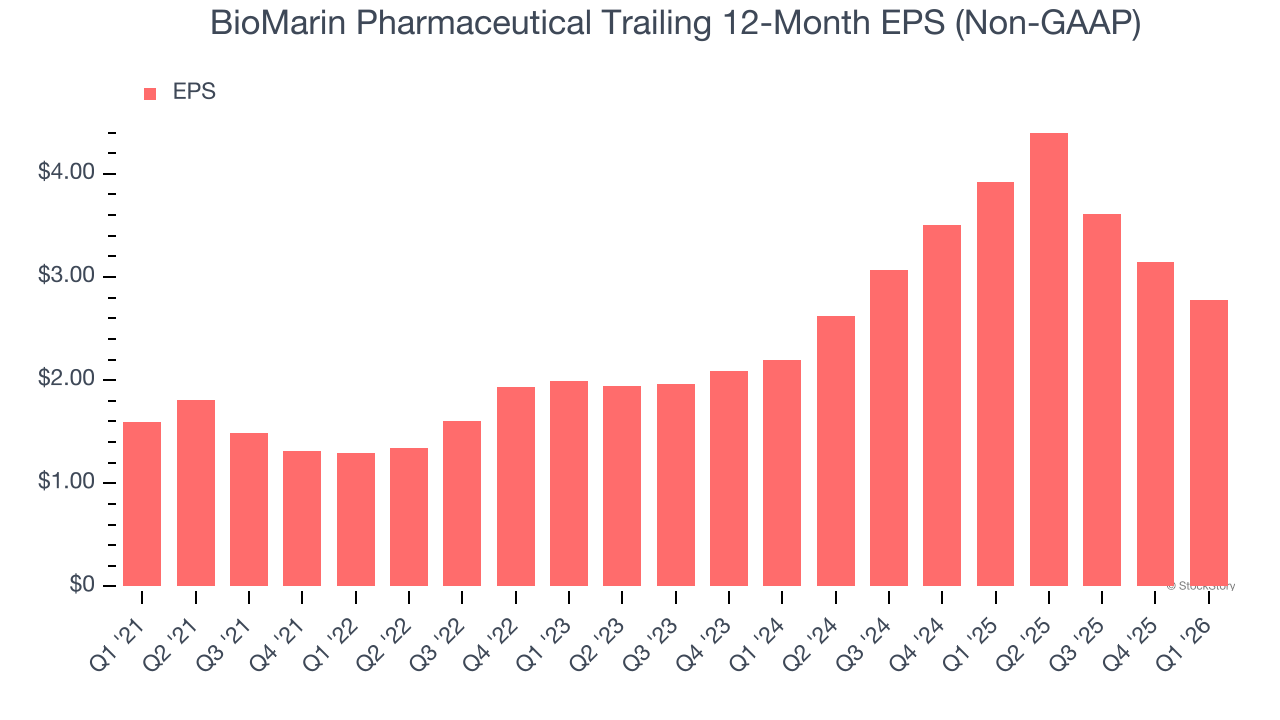

BioMarin Pharmaceutical’s remarkable 11.7% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

In Q1, BioMarin Pharmaceutical reported adjusted EPS of $0.76, down from $1.13 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from BioMarin Pharmaceutical’s Q1 Results

We were impressed by how significantly BioMarin Pharmaceutical blew past analysts’ full-year EPS guidance expectations this quarter. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its EPS missed and its revenue fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $54.93 immediately following the results.

Is BioMarin Pharmaceutical an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).