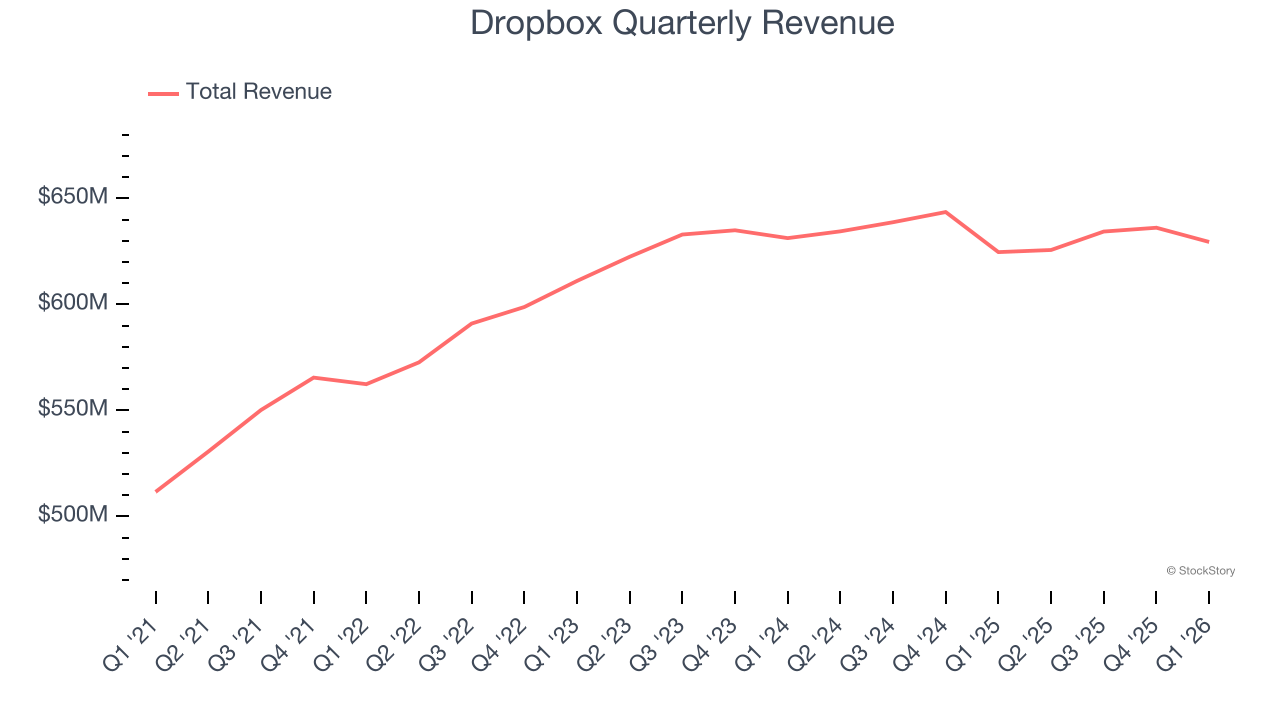

Cloud storage company Dropbox (NASDAQ: DBX) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, but sales were flat year on year at $629.5 million. Its non-GAAP profit of $0.76 per share was 9.1% above analysts’ consensus estimates.

Is now the time to buy Dropbox? Find out by accessing our full research report, it’s free.

Dropbox (DBX) Q1 CY2026 Highlights:

- Revenue: $629.5 million vs analyst estimates of $620.9 million (flat year on year, 1.4% beat)

- Adjusted EPS: $0.76 vs analyst estimates of $0.70 (9.1% beat)

- Adjusted Operating Income: $252.2 million vs analyst estimates of $235.9 million (40.1% margin, 6.9% beat)

- Operating Margin: 27.5%, down from 29.4% in the same quarter last year

- Free Cash Flow Margin: 32.3%, down from 35.4% in the previous quarter

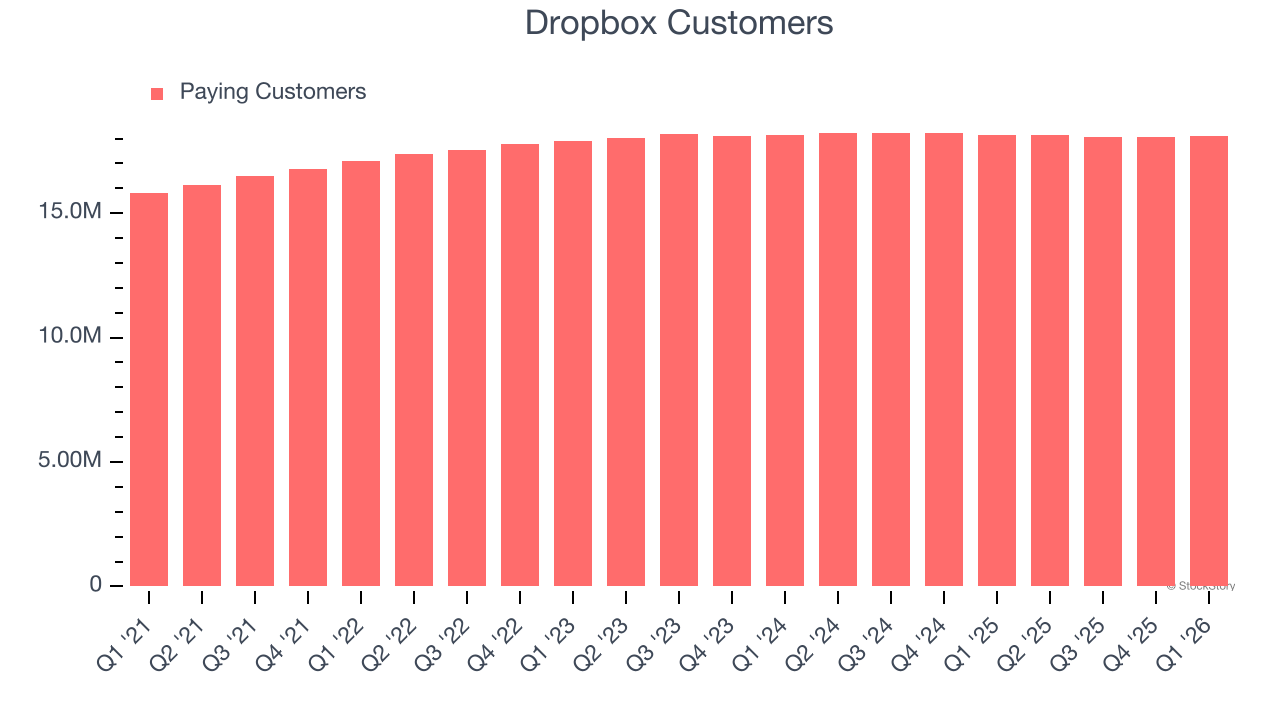

- Customers: 18.09 million, up from 18.08 million in the previous quarter

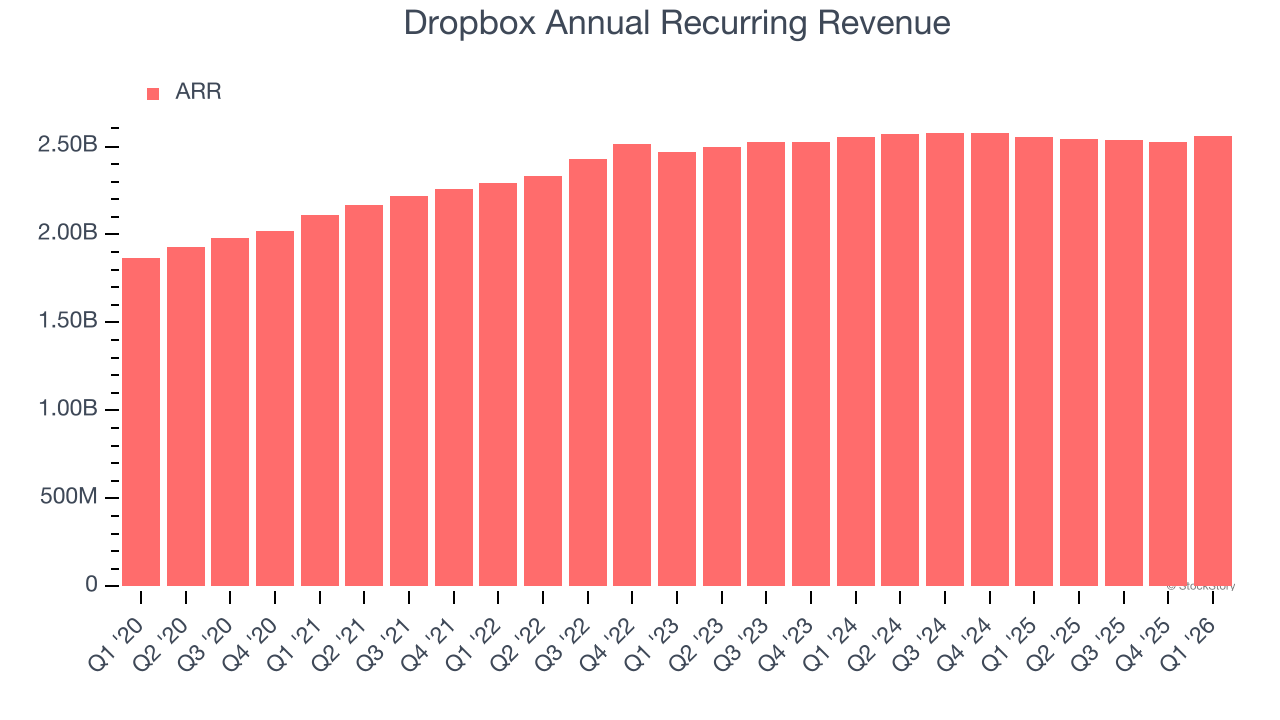

- Annual Recurring Revenue: $2.56 billion (flat year on year, beat)

- Billings: $647.5 million at quarter end, up 1.7% year on year

- Market Capitalization: $5.89 billion

Company Overview

Originally named after the founders' tendency to "drop" files into a shared folder, Dropbox (NASDAQ: DBX) provides a content collaboration platform that helps individuals and teams store, organize, share, and work on files from anywhere.

Revenue Growth

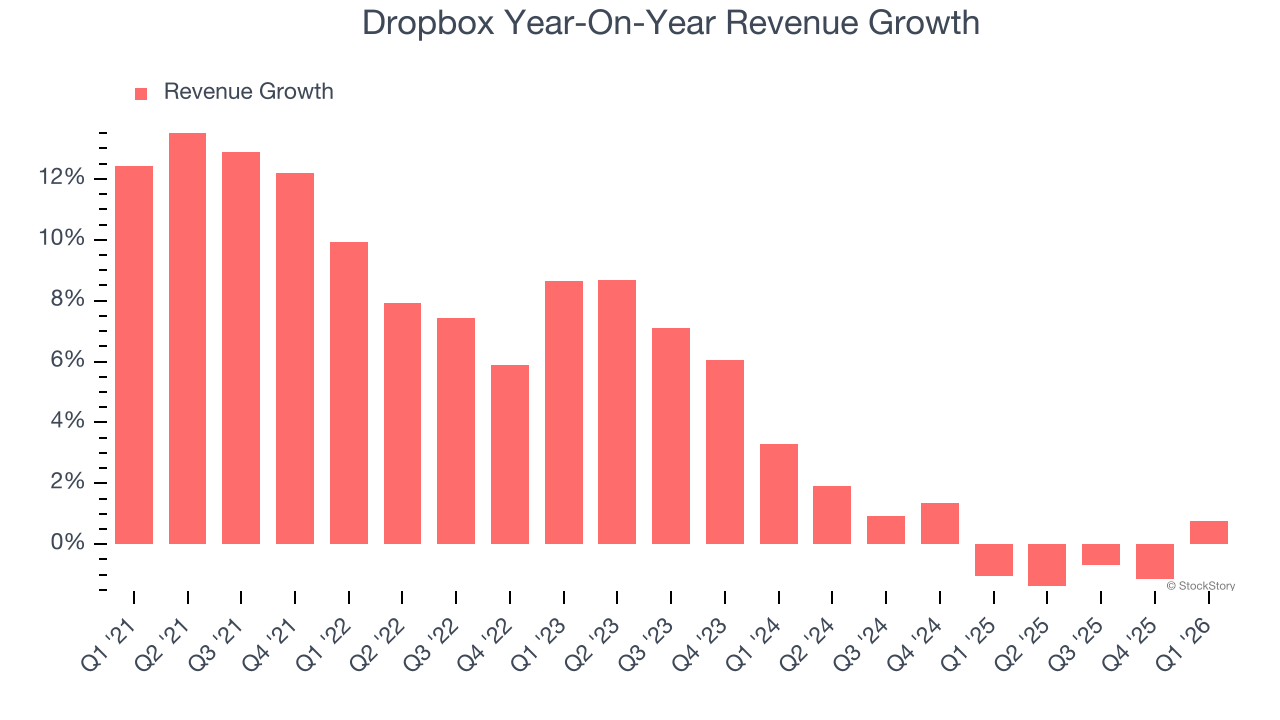

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Dropbox grew its sales at a weak 5.1% compounded annual growth rate. This was below our standard for the software sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Dropbox’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Dropbox’s $629.5 million of revenue was flat year on year but beat Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to decline by 1.2% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its products and services will see some demand headwinds.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Dropbox’s ARR came in at $2.56 billion in Q1, and it averaged 1.1% year-on-year declines over the last four quarters. This performance mirrored its total sales, showing the company lost long-term deals and renewals. It also suggests there may be increasing competition or market saturation.

Customer Base

Dropbox reported 18.09 million customers at the end of the quarter, a sequential increase of 10,000. That’s roughly in line with what we observed last quarter and quite a bit above what we’ve seen over the previous year. Shareholders should take this as an indication that Dropbox has made some recent improvements to its go-to-market strategy.

Key Takeaways from Dropbox’s Q1 Results

We enjoyed seeing Dropbox beat analysts’ billings expectations this quarter. We were also happy its annual recurring revenue narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 2.7% to $25.78 immediately after reporting.

Dropbox put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).