What a brutal six months it’s been for Cadre. The stock has dropped 29.5% and now trades at $30.19, rattling many shareholders. This may have investors wondering how to approach the situation.

Following the drawdown, is this a buying opportunity for CDRE? Find out in our full research report, it’s free.

Why Does Cadre Spark Debate?

Originally known as Safariland, Cadre (NYSE: CDRE) specializes in manufacturing and distributing safety and survivability equipment for first responders.

Two Positive Attributes:

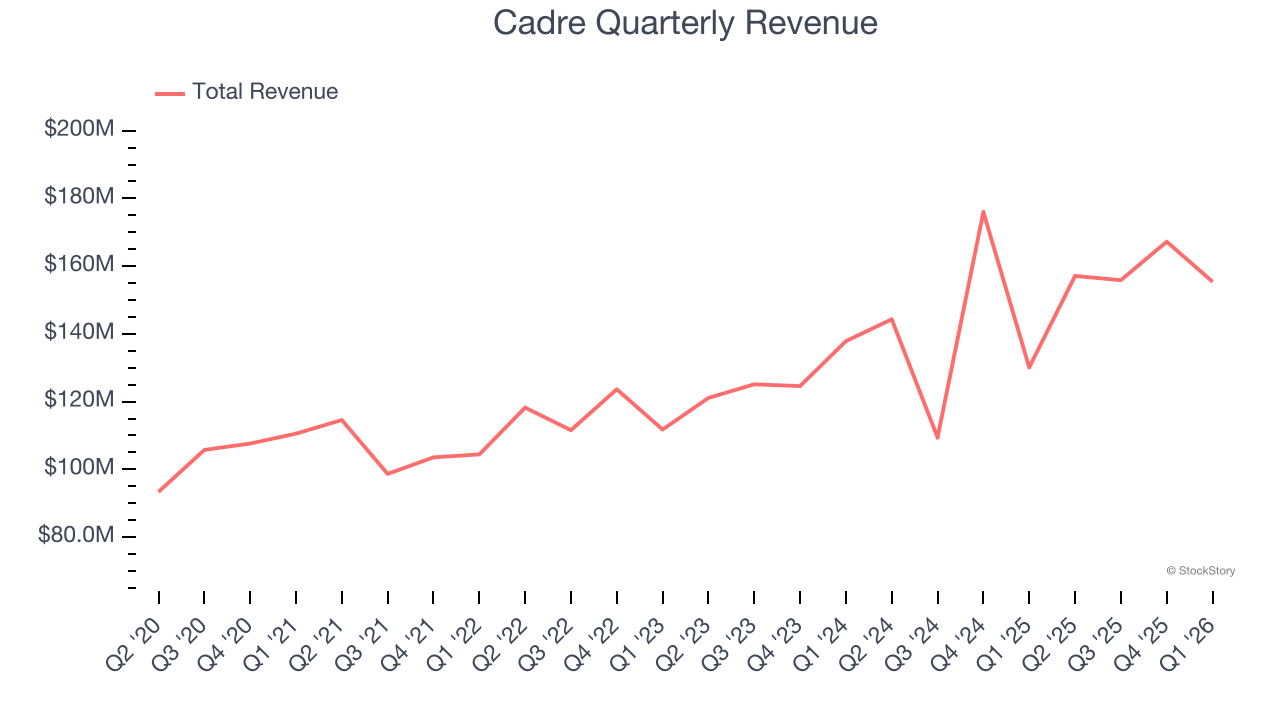

1. Long-Term Revenue Growth Shows Momentum

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Cadre’s 8.8% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Cadre’s revenue to rise by 17.6%, an improvement versus its 8.8% annualized growth for the past five years. This projection is eye-popping and indicates its newer products and services will catalyze better top-line performance.

One Reason to Be Careful:

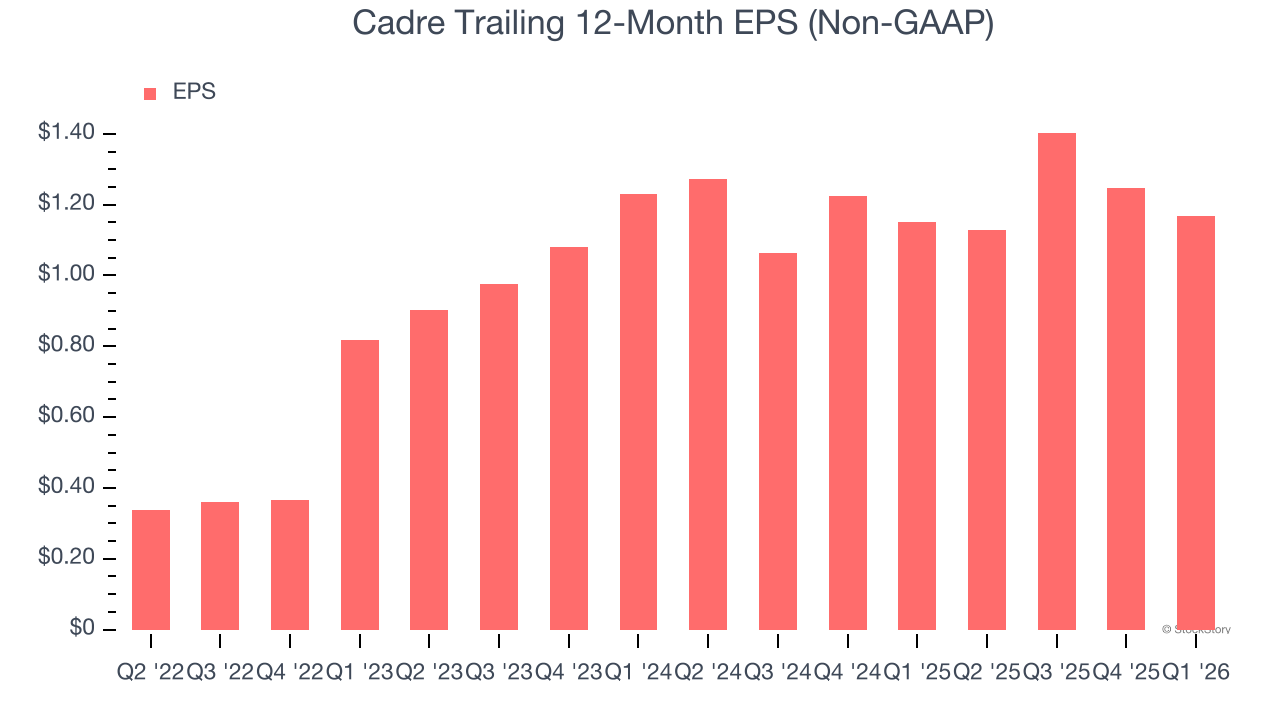

EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Cadre, its EPS declined by 2.6% annually over the last two years while its revenue grew by 11.8%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Cadre’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at $30.19 per share (or a forward price-to-sales ratio of 1.7×). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Cadre

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.