Warby Parker has been treading water for the past six months, recording a small loss of 1.5% while holding steady at $26.43. The stock also fell short of the S&P 500’s 8.4% gain during that period.

Is there a buying opportunity in Warby Parker, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Warby Parker Not Exciting?

We’re cautious about Warby Parker. Here are three reasons we avoid WRBY, plus one stock we’d rather own.

1. Fewer Distribution Channels Limit Its Ceiling

With $890.6 million in revenue over the past 12 months, Warby Parker is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers. On the bright side, it can grow faster because it has more white space to build new stores.

2. Operating Losses Sound the Alarm

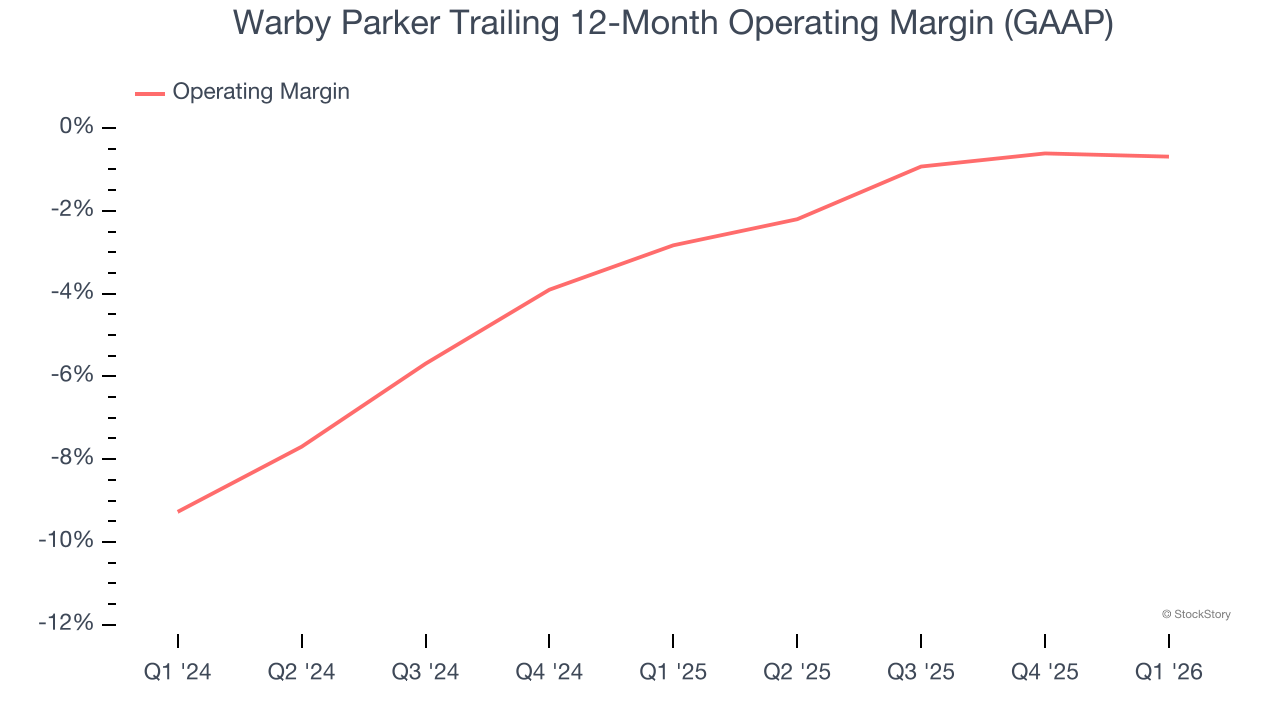

Operating margin is a key profitability metric because it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Although Warby Parker broke even this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 1.7% over the last two years. Despite the consumer retail industry’s secular decline, unprofitable public companies are few and far between. It’s unfortunate that Warby Parker was one of them.

3. Previous Growth Initiatives Have Lost Money

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Warby Parker’s four-year average ROIC was negative 41.4%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer retail sector.

Final Judgment

Warby Parker isn’t a terrible business, but it doesn’t pass our bar. With its shares trailing the market in recent months, the stock trades at 50.4× forward P/E (or $26.43 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d suggest looking at the most entrenched endpoint security platform on the market.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.