Snap (SNAP) is once again in the spotlight. The company just announced that it will cut 1,000 jobs, or about 16% of its workforce, as it pushes hard toward profitability in 2026. The move comes as Snap joins a growing list of tech firms trimming their headcounts while leaning into artificial intelligence (AI) to run operations. Meta Platforms (META), Amazon (AMZN), and Oracle (ORCL) have all made similar moves recently.

Now, Snap is betting that AI can replace repetitive work and help it scale faster with fewer people. The layoffs are not just about cutting expenses. They are about reshaping the entire cost structure.

According to CEO Evan Spiegel, Snap expects to save around $500 million annually from the restructuring. Investors liked the news, and SNAP stock surged 8% on April 15 following the restructuring announcement. In short, Snap is cutting costs to survive and trying to prove it can finally turn scale into profit.

Snap Doubles Down on AI Push to Boost Efficiency

Snap is a technology and social platform company best known for Snapchat. It focuses on messaging, augmented reality (AR) filters, and short-form content. Over the years, it has tried to expand into AR hardware, subscriptions, and digital ads, but profitability has remained inconsistent.

Snap is also making structural changes in 2026. The company is pushing harder into AI-driven ad targeting, expanding Snapchat+ subscriptions, and scaling its AR ecosystem for advertisers. Internally, it is already using AI tools to automate parts of coding and ad optimization, which management says is improving productivity significantly.

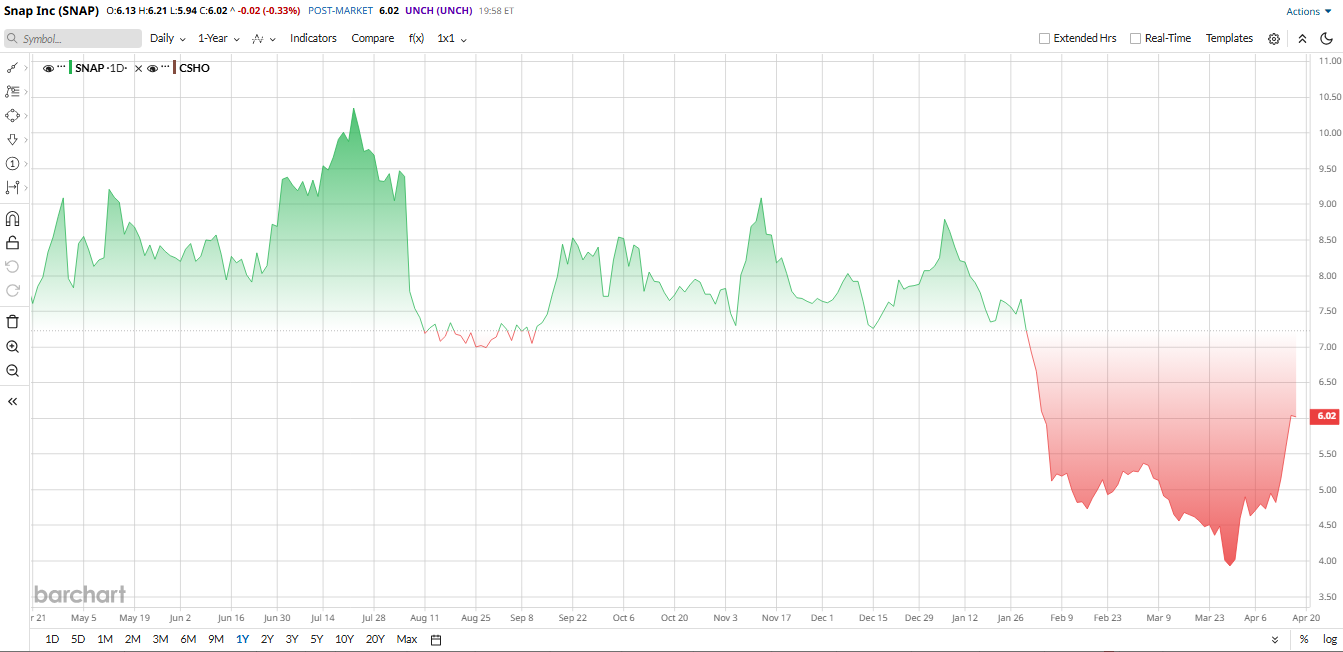

Despite seeing a bump on the layoff news, shares of Snap are down more than 26% down year-to-date (YTD) due to weak ad trends and competitive pressure from Meta and TikTok. SNAP stock is still trading above its key 50-day moving average, while the 200-day trend continues to act as resistance.

On the valuation front, Snap does not look expensive on traditional revenue metrics. It trades at roughly 1.7 times sales, slightly below the social media sector median closer to 3 times. However, on earnings-based multiples, it still screens as stretched because profitability is inconsistent. It is not cheap enough to be a clear value play, but not strong enough to justify a premium, either.

A Look at the Latest Numbers

Snap reported its fourth-quarter 2025 results on Feb. 4, showing steady revenue growth as digital advertising and subscription gains supported performance. Revenue came in at about $1.72 billion, up roughly 10% year-over-year (YOY), driven by stronger ad demand and continued growth in Snapchat+ subscriptions. Early traction in AR-based advertising tools also supported results, although ad spending trends remained uneven across key regions.

Adjusted net income was slightly positive, with EPS of $0.03 improving from $0.01 in the same period last year. Free cash flow totaled about $205 million, a rebound from prior cash burn phases. Cash and equivalents stood at roughly $2.9 billion, giving Snap flexibility to continue restructuring without near-term funding pressure.

Looking ahead, Snap expects mid single-digit to low double-digit revenue growth next quarter, along with further improvement in adjusted EBITDA margins. Analysts forecast full-year 2026 revenue between $6.3 billion and $6.6 billion, with earnings still hovering near breakeven as investors watch for sustained margin expansion.

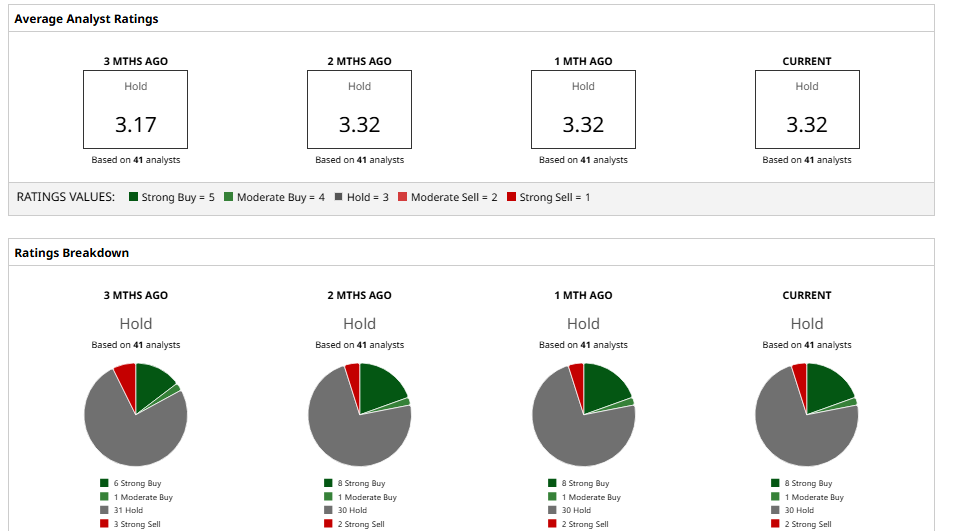

Wall Street Opinions Remain Mixed

Wall Street isn’t exactly aligned on SNAP stock right now, but the numbers make the picture clearer.

Morgan Stanley is cautious on Snap. The firm recently cut its price target to $6.50 from $9.50 and maintained an “Equal Weight” rating. That implies roughly 9% potential upside from current levels, reflecting limited conviction despite potential margin improvement.

Goldman Sachs is also “Neutra” on shares. It lowered its target to $8.50 from $9.50. The firm still sees uneven ad demand and slow recovery trends.

JPMorgan is even more cautious, however. The firm cut its target to $7 from $8 and kept an “Underweight” rating, implying about 18% potential upside but with continued concerns about long-term ad share losses.

Zooming out, the broader picture is clear. Snap has a "Hold" consensus rating based on 41 analysts with coverage. The average price target sits at $8.14. At recent prices, that implies roughly 37% potential upside from here.

Analysts seem to agree on one thing: Snap isn’t broken, but it isn’t proven, either.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Costco Raises Its Dividend More Than 13%, Should You Buy, Sell, or Hold COST Stock?

- Tilray Stock Pops on New Trump-Driven Cannabis Hopes. Should You Chase the Rally?

- Tim Cook Is Stepping Down as Apple CEO, AAPL Stock Dips in After-Hours Trading

- Save This Psychedelic Stock Watchlist After Trump’s Latest Executive Order