Dividend yield is the preferred metric for choosing dividend stocks. However, the equation has two moving parts. While, preferably, dividend yield should go up when companies increase dividends (or the numerator), quite often the opposite is true, and the yield rises when the stock falls and pulls down the denominator in the equation.

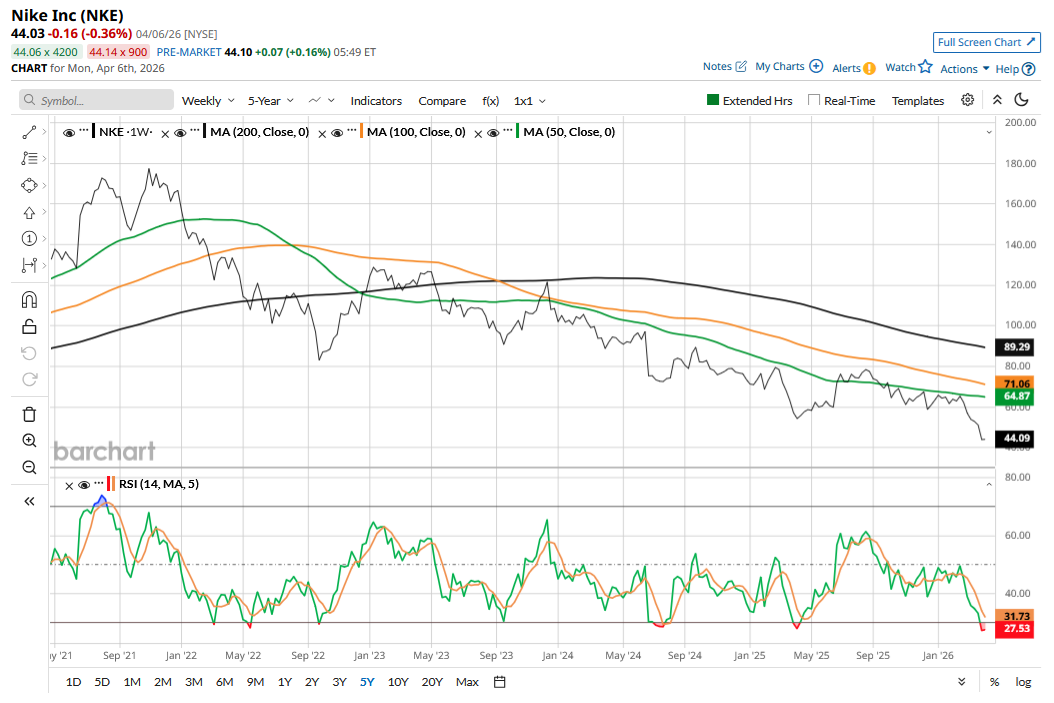

Nike (NKE) is a case in point here. The sneaker giant’s stock is trading at an 11-year low, which has pushed up its dividend yield to an all-time high of over 3.7%. The company currently pays a quarterly dividend of 41 cents, which was last raised by 2.5% last year. It has a formidable track record on dividends and has increased them for 24 consecutive years. Repeating the feat for one more year will make Nike a Dividend Aristocrat.

Meanwhile, the dividend yield doesn’t mask the massive capital erosion, with NKE stock having lost two-thirds of its market cap over the last three years. Is NKE stock a buy for its dividend, or would investors be better off staying away from the troubled company? Let’s explore, beginning with the company’s dividend.

Is Nike’s Dividend Sustainable?

Companies with high dividend yields often tend to be in trouble, so it is prudent to examine the sustainability of the payouts. In Nike’s case, its payout ratio has surpassed 100%, which basically means that the dividends are higher than its earnings. More worrisome is that, in fiscal Q3 2026, which ended in February, its dividend payments exceeded its operating free cash flow. The company's cash pile eroded by a massive $2.3 billion in the quarter, as, apart from dividends, it spent on capex, bond repayments, and share repurchases.

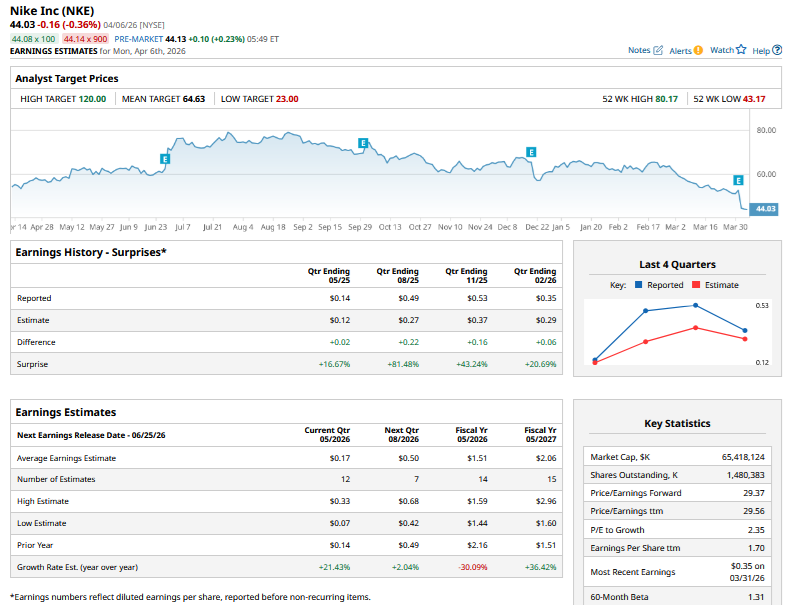

Looking at the trailing numbers, Nike’s dividends would look unsustainable. However, the company’s profitability and margins should improve in the coming quarters. Consensus estimates call for a 21.4% increase in the current quarter’s earnings per share (EPS), which is the last quarter of Nike’s fiscal year. For the next fiscal year, analysts are modeling a 36.4% rise.

To be sure, these are estimates and are subject to revision as things evolve. However, I am on the same page as Nike and the analyst community that the worst is nearly over for the company, at least in terms of profitability.

Considering the expected increase in profitability, Nike’s dividends would appear sustainable. Also, slashing dividends would be quite a drastic move, and while it helps conserve cash, such a decision might not be taken kindly by the markets. To sum it up, Nike’s dividends look sustainable to me unless the slump in the company’s earnings continues for an extended period, something whose probability is quite low.

Should You Buy NKE Stock?

However, dividends are usually a side story, or in Nike’s case, let’s say supporting cast. The real bet is on Nike's turnaround, which is taking painfully long. As CEO, Elliott Hill reportedly told employees at a recent all-hands meeting, “I’m so tired, and I know you are too, of talking about fixing this business.”

Nike’s problems are multifold, as the company hasn’t fully evolved to meet customer needs and aspirations. In an era where celebrity and influencer brands are getting popular and newer brands are riding the social media wave to gain traction, Nike slackened on innovation—something the company itself admitted. As fellow Barchart analyst Jim Osman aptly wrote, Nike’s problem is “relevance.” The brand is also not as strong as the company perceived it to be, and it had to rebuild relations with third-party sellers and wholesalers after previously ditching them for direct sales.

Meanwhile, even as Nike is currently going through turmoil, it still does not look like a company in terminal decline. After Nike’s fiscal Q3 earnings release, I had noted that the stock needs to fall more to appear attractive. NKE stock has plunged sharply after that earnings report, and the market cap is just about $65 billion now.

Nike trades at a forward price-to-earnings (P/E) multiple of 29.4x, which wouldn’t appear too cheap. However, analysts expect it to post an EPS of $2.57 in fiscal year 2028, which gives us a FY28 P/E of just over 17x. However, as stated previously, these are only estimates, and Nike remains a “show me” story that has to deliver on the turnaround.

Overall, I believe that after the sharp fall, Nike’s risk-reward is a lot more balanced now, even if it's not a compelling buy yet, given the adverse macro environment.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Wannabe Dividend Aristocrat Yields Nearly 4%: Should You Buy?

- 2 Energy Stocks That Are Quietly Winning This Crisis

- Raytheon Is a Top Defense Stock to Buy Amid the Iran War, But It Will Also Benefit From a Ceasefire. Here’s How.

- 3 Dividend Kings With 50+ Years of Raises Are Trading at a Huge Discount. Analysts Say Buy Before They Rebound