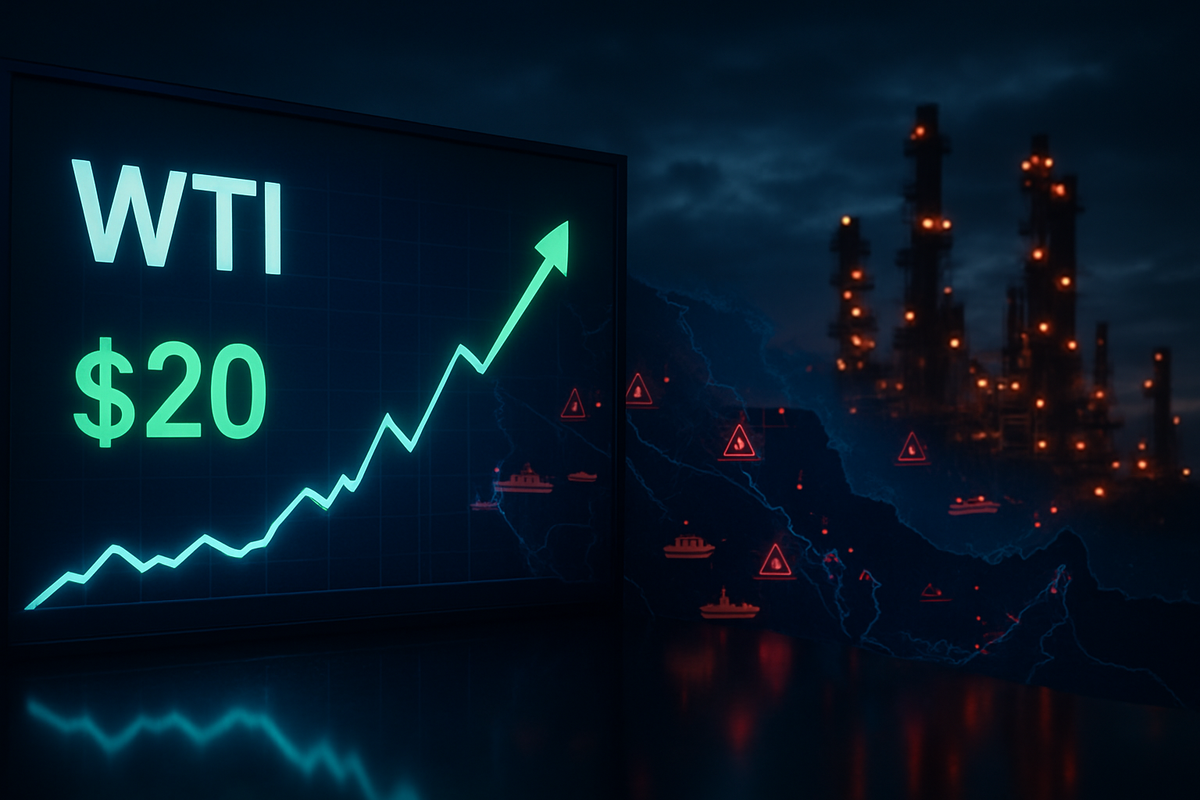

In a move that has sent tremors through global financial markets, the U.S. Energy Information Administration (EIA) has aggressively revised its 2026 price forecast for West Texas Intermediate (WTI) crude oil, raising its average spot price projection by a staggering $20 per barrel. This massive upward adjustment, detailed in the agency’s March 2026 Short-Term Energy Outlook (STEO), marks one of the most significant month-over-month shifts in the agency’s history, reflecting a world suddenly gripped by a "geopolitical risk premium" that many analysts thought had been relegated to the past.

The revision comes on the heels of a rapid escalation in Middle Eastern hostilities that began in late February, leading to the effective closure of the Strait of Hormuz—a vital artery through which 20% of the world’s oil supply flows. With the EIA now projecting WTI to average $73.61 for the full year 2026—up from a previous estimate of $53.42—and peak prices already testing the $100 mark in April, the global economy is bracing for a sustained period of energy-driven inflation and supply-chain volatility.

From Stability to Siege: The $20 Revision

The catalyst for this drastic forecast change was the "Iran War Shock," which ignited on February 28, 2026. The conflict, involving a series of maritime skirmishes and missile strikes across the Persian Gulf, culminated on March 4 when the Strait of Hormuz became impassable for commercial tankers. While physical infrastructure remained largely intact, the loss of shipping insurance and the threat of targeted attacks essentially "shut in" millions of barrels of production from Iraq, Kuwait, the UAE, and Saudi Arabia. The EIA’s March STEO was the first official government acknowledgment that these disruptions were not a momentary glitch but a structural shift in the 2026 energy landscape.

Timeline data suggests that the EIA finalized its revised figures just as Brent crude spiked toward $119 per barrel in early March. The agency’s modeling now assumes that even if a diplomatic resolution is reached, the "normalization" of shipping routes will be a protracted process extending into late 2026. The forecast highlights a particularly brutal second quarter, with WTI expected to average $91 in March and $89 in April. This "supply shock" scenario has forced the EIA to rethink the global balance, as it now expects Middle Eastern output to remain volatile while Western producers scramble to fill the void.

Initial market reactions have been frantic. Global CPI inflation forecasts for 2026 have already been hiked to 4.0%, while global GDP growth projections have been trimmed to 2.6% from a previous 3.0%. Central banks, which had been signaling a shift toward easing, are now caught in a "stagflationary" pincer, weighing the need to combat rising energy costs against a slowing industrial sector. The EIA’s revision serves as the official starting gun for a year where energy security will dominate every boardroom and policy debate.

The Crude Divide: Corporate Winners and Losers

The surge in crude prices has created a stark bifurcation in the equities market, favoring upstream giants while punishing fuel-intensive industries. Occidental Petroleum (OXY:NYSE) has emerged as the standout performer of the first quarter, with its stock rallying 50% year-to-date as of late March. As a "pure-play" upstream producer with a dominant footprint in the Permian Basin, Occidental is perfectly positioned to capture the triple-digit price environment. The company recently capitalized on the momentum by selling its chemicals business to Berkshire Hathaway (BRK.B:NYSE) for $9.7 billion, a strategic pivot to focus entirely on maximizing its shale output and retiring debt during this windfall period.

Similarly, ExxonMobil (XOM:NYSE) has seen its shares jump 36% year-to-date, trading near record highs of $171. Exxon has already signaled a 12.5% production increase in the Permian Basin for 2026, aiming for 1.8 million barrels of oil equivalent per day. By contrast, the aviation sector is reeling. Delta Air Lines (DAL:NYSE) and American Airlines (AAL:NASDAQ) have both reported staggering hits to their bottom lines, with Delta confirming an additional $400 million in fuel expenses for March alone. While airlines have attempted to pass these costs to consumers via international fuel surcharges and 15–20% hikes in domestic base fares, the risk of "demand destruction" looms large if ticket prices continue to climb alongside gasoline.

The Return of the Risk Premium

This event signals a fundamental shift in broader industry trends, effectively ending the era of "low for longer" oil prices that characterized much of the early 2020s. For years, the market had discounted the possibility of a total closure of the Strait of Hormuz, assuming that the global transition toward renewables would dampen the impact of Middle Eastern instability. The EIA’s $20 revision is a cold shower for that narrative, proving that the world remains precariously dependent on fossil fuel chokepoints. This "Hormuz Premium" is now being baked into long-dated futures contracts, suggesting that volatility will persist even if the shooting stops.

Historically, this event mirrors the oil shocks of the 1970s and the 2011 Arab Spring, but with a modern twist: the U.S. is now the world’s leading producer. This has created a geopolitical paradox where the U.S. economy is simultaneously protected by its domestic production and threatened by the global inflationary pressure of high oil. Regulatory focus is already shifting, with calls in Washington to fast-track permits for LNG terminals and offshore drilling to provide a "security buffer" for European and Asian allies who are currently cut off from Gulf supplies.

The Path to a 15-Point Peace?

The short-term outlook hinges on the success of a "15-point ceasefire plan" currently being discussed between the U.S. and regional powers. A "relief rally" on March 31, 2026, saw oil prices pull back slightly from their peaks, but the market remains skeptical. For energy companies, the strategic pivot is clear: maximize production now while the "price window" is open. We are likely to see a surge in CAPEX toward "short-cycle" assets like shale, which can be brought online in months rather than years.

In the long term, if the Strait remains contested, we may see a permanent redirection of global trade. Saudi Arabia is already looking to maximize its alternative export conduits to the Red Sea, though these are also under threat from regional proxies. Investors should prepare for a "bumpy plateau" in prices rather than a clean return to $50 oil. If the ceasefire fails, $120 WTI is no longer a "tail risk"—it is a baseline scenario.

Navigating the New Energy Reality

The EIA’s $20 forecast revision is more than just a number; it is a recognition that the global energy map has been redrawn. The key takeaway for investors is that the "geopolitical risk premium" has returned with a vengeance, and it is likely to stay as long as the Strait of Hormuz remains a flashpoint. While companies like Chevron (CVX:NYSE) and Diamondback Energy (FANG:NASDAQ) stand to benefit from a sustained high-price environment, the broader market must contend with the cooling effect of $4-per-gallon gasoline and $100-per-barrel feedstock.

Moving forward, the market will be hyper-focused on two metrics: weekly rig counts in the Permian Basin and the status of shipping insurance in the Persian Gulf. If U.S. production can scale fast enough, it may take the top off the price spike, but it cannot replace the 20 million barrels per day that flow through Hormuz. For now, the "Iran War Shock" has put the energy transition on the back burner, as "energy security" becomes the defining investment theme of 2026.

This content is intended for informational purposes only and is not financial advice.